When Justin Trudeau and the Liberal Party won a majority of seats in the Canadian Parliament elections in October last year, it set off a quick pop in the stocks of several licensed producers (LPs) of cannabis under the MMPR medical cannabis program administered by Health Canada, as investors began to price in the likelihood of legalization for adult use given the campaign promises of the party. The burst in prices proved somewhat short-lived, but the sector has exploded to new highs since the end of June as it has become increasingly clear that the country is on track to become the first G-7 nation to legalize cannabis for adults.

In late December, we announced the creation of an index to track the sector. The index includes all publicly-traded licensed producers and gives extra weight for those with sales that exceed a threshold. Initially, there were seven members, but, with two additional companies gaining licensing subsequently, the index now includes nine companies. The progression of the index is here.

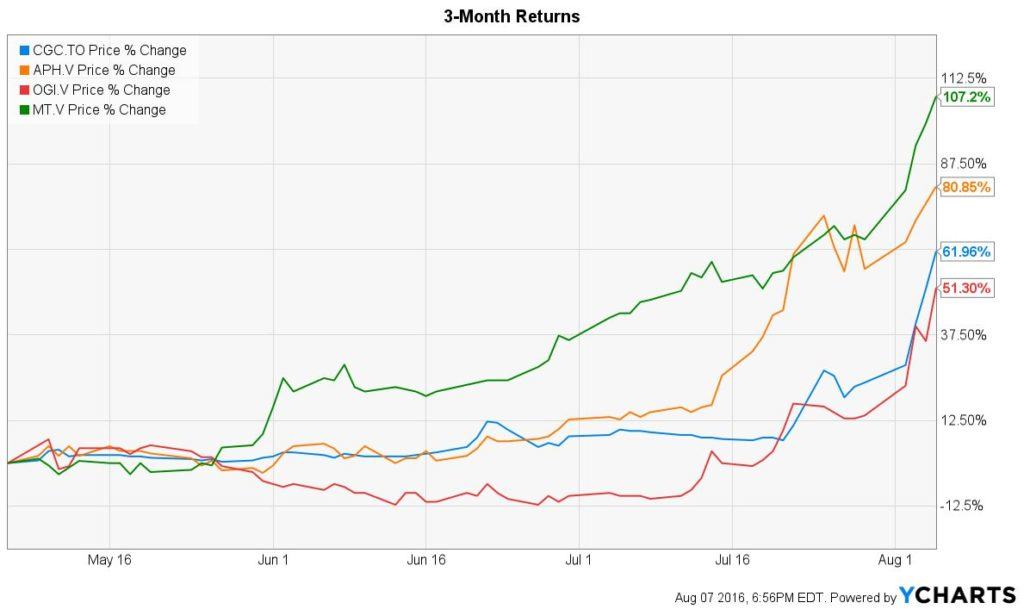

Through August 5th, the index, which jumped 29.1% last week, has increased 60.9% YTD after having been down 1.5% through June. I am proud to say that the 420 Investor Canadian Cannabis model portfolio that I share with my subscribers has increased 82.0% YTD. Here are the returns YTD for each of the nine members in descending order. Note that Supreme Pharma and THC Biomed were not included in the index at the beginning of the year because they had not yet received their cultivation license.

- Aphria (TSXV: APH) (OTCQB: APHQF): +99.2%

- THC Biomed (CSE: THC) (OTC: THCBF): +94.7%

- Organigram (TSXV: OGI) (OTC: OGRMF): +85.1%

- Mettrum (TSXV: MT) (OTC: MQTRF): +66.8%

- PharmaCan Capital (TSXV: MJN) (OTC: PRMCF): +58.7%

- Canopy Growth (TSX: CGC) (OTC: TWMJF): +39.1%

- Emerald Health (TSXV: EMH) (OTC: TBQBF): +22.7%

- Aurora Cannabis (CSE: ACB) (OTC: ACBFF): +10.0%

- Supreme Pharma (CSE: SL) (OTC: SPRWF): -2.0%

The rise in prices has been fueled by several factors. In mid-June, when only three stocks in the group were up YTD, we wrote about three reasons investors should focus on the sector:

- Medical cannabis is federally legal, and Canada will soon become the first regulated federally legal market for adult consumption among major countries

- Canadian companies have good access to capital

- Prices have pulled back in front of catalysts ahead

As the summer has progressed, there have been several favorable events. Continued crackdowns against illegal dispensaries in Ontario have given investors comfort that the LPs will be supported by the government. Additionally, Canopy Growth, which operates Bedrocan Cannabis and Tweed, was able to uplist from the TSX Venture to the TSX, while Aphria gained an OTCQB listing in the United States, both of which point to better liquidity and a widening investor base. Perhaps most importantly, though, patient growth in the MMPR program exploded, with leaders Canopy Growth and Mettrum providing details of substantial registered patient growth into late June as we reported then. Finally, the creation of a task force and the issuance of its initial report on June 30th, offering a timeline for issuing a report by November that will be used as the basis for the legislation to be introduced in the first half of 2017, served to highlight how much closer Canada is to legalization.

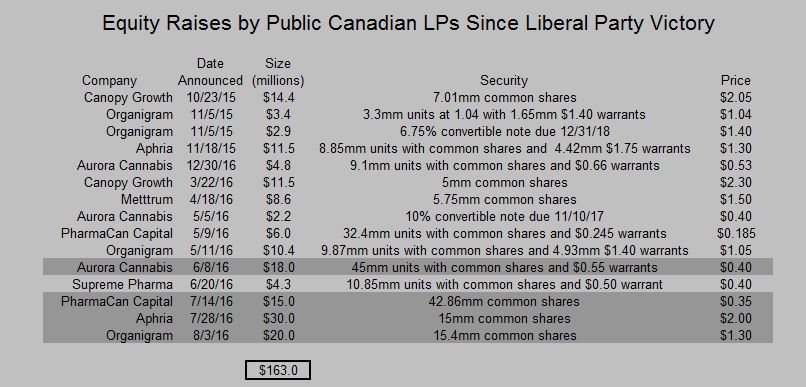

As a result of rising stock prices and driven by the need for more capacity to serve the much larger legal market beginning in 2018, the LPs have continued to raise capital. In the last three weeks, deals totaling $65mm have been announced.

The shaded deals haven’t yet closed. Aphria and Organigram are both “bought” deals, each having an underwriters’ option that could increase the size. PharmaCan is a private placement that was announced in conjunction with the disclosure of a pending acquisition of Peace Naturals. Aurora Cannabis may increase the size of its private placement, which is being managed by Canaccord.

Health Canada agreed in February to revise the MMPR Program following the Allard case decision declaring it to be unconstitutional because it restricts access. The revisions are due by August 24th, and it is very likely that some form of home grow will be permitted. Hugo Alves shared his extensive views of what to expect, and several LP CEOs weighed in last week as well. In addition to the Health Canada response within the next few weeks, Canopy Growth and Mettrum, the two publicly-traded LPs with the most number of registered patients, will report their financials for their FY17-Q1 ending June 30th before the end of the month.

Investor focus on the Canadian LPs has sharpened, and the long-term industry opportunity appears to be substantial. The details of legalization won’t be revealed until the November task force report, but it seems extremely likely that the existing LPs will play a big role. Still, investors should consider that the supply chain will likely expand, with distribution almost certain to move from beyond exclusively mail-order to one with physical store-fronts, particularly pharmacies but also other entities that extend beyond the current supply chain. Another near-term risk factor is that the Veterans Affairs Canada could reduce the price reimbursement and the prescription sizes for veterans, a potential near-term setback for certain LPs. Despite the potential for near-term volatility, especially after the sharp rise in prices so far this quarter, the long-term outlook for the Canadian LPs is positive.