As we described in a previous article, the Global Cannabis Stock Index fell in February after rising to begin the year. The index declined 6.3% after a 10.1% gain in the prior month following a record decline of 70.4% for 2022.

In this exclusive article we will summarize the performance of the other managed indices that New Cannabis Ventures offers to its readers. We will discuss the performance of the American Cannabis Operator Index, Ancillary Cannabis Index and Canadian Cannabis LP Index as well as Canadian Cannabis LP index Tier 1, 2 and 3.

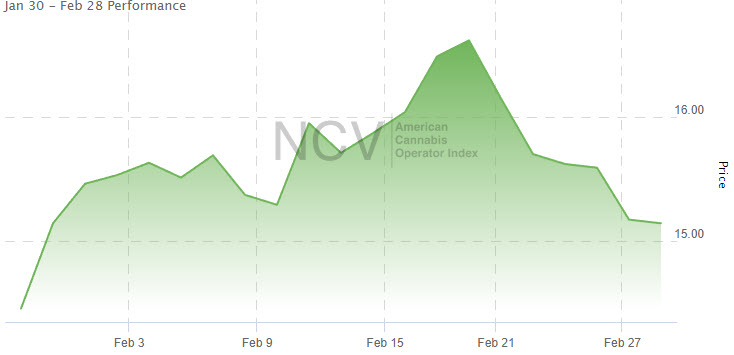

American Cannabis Stocks Index

The American Cannabis Operator Index was one of the weakest parts of the market in January, but it was relatively strong in February when it was unchanged at 15.14. It is up 6.3% in 2023:

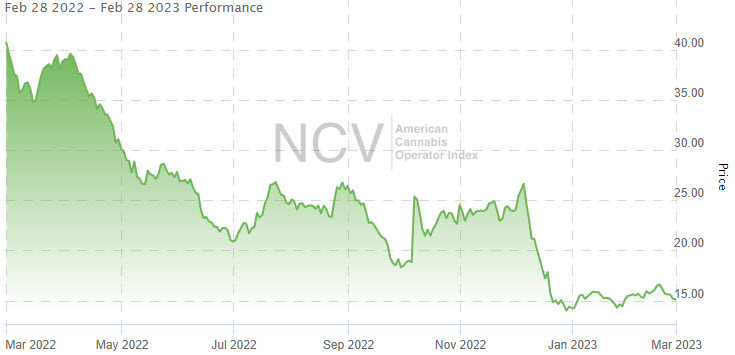

Down 22.9% in Q4 after a collapse in December, it was down 65.8% in 2022 to 14.25, slightly ahead of the Global Cannabis Stock Index. Over the past year, the index has declined 62.8%:

The index, which launched in October 2018, finally took out the low from March 2020 in late 2022:

During February, two stocks were double-digit gainers, TerrAscend (OTC: TRSSF) (CSE: TER), up 14.0%, and Glass House Brands (OTC: GLASF) (NEO: GLAS.A.U), up 12.3%. Ayr Wellness (OTC: AYRWF) (CSE: AYR.A) fell 11.8%.

In March, the index will decline to 11 members with the deletions of MariMed (OTC: MRMD) (CSE: MRMD) and Planet 13 Holdings (OTC: PLNHF) (CSE: PLTH) and the addition of Upexi (NASDAQ: UPXI).

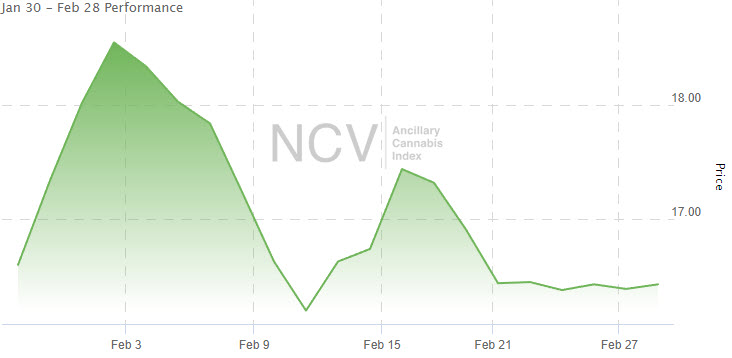

Ancillary Cannabis Index

The Ancillary Cannabis Index fell 5.3% to 16.43, up 9.4% in 2023:

The index, up 15.5% in January after a massive loss of 76.6% in 2022 to 15.02, has declined 68.1% over the past year:

The index is down almost 84% since launching at the end of March in 2021:

During February, one stock rallied a lot, and four stocks fell by more than 10%. Scotts Miracle-Gro (NYSE: SMG) rose 14.3%, while Agrify (NASDAQ: AGFY) fell 23.0%. The other stocks that were all down more than 11%, included GrowGeneration (NASDAQ: GRWG), WM Technology (NASDAQ: MAPS) and AgriFORCE Growing (NASDAQ: AGRI).

In March, the index will drop to just 8 members. Leaving due to insufficient trading volume are Agrify, which also fell below the minimum price, AgriFORCE Growing and WM Technology.

Canadian Cannabis LP Index

The Canadian Cannabis LP Index was very strong to begin the year, rising 19.4% in January to 86.64. In February, it fell slightly to 85.84, down 0.9%:

The index, down 11.4% in Q4 , declined 62.8% in 2022 to 72.59. It is up 18.3% so far in 2023. Over the last year, it has dropped now by 50.0%.

The index, which made a new all-time low in December, is down a lot from its peak:

Canadian Cannabis LP Tier 1 Index

During January, Tier 1 surged 23.9%, but it gave up 10% in February, dropping to 98.21. Tier 1 was down 72.0% in 2022, ending at 88.14, and it is up 11.4% in 2023. Among Tier 1 companies, HEXO Corp. (TSX: HEXO) (NASDAQ: HEXO) was the best performer again, rising 10.9%. The worst Tier 1 stock in January was Canopy Growth (TSX: WEED) (NASDAQ: CGC), falling 21.3%.

Canadian Cannabis LP Tier 2 Index

Tier 2 index gained 7.5% in January, and it dropped 7.4% in February to 109.29. In 2022, it lost 58.9%, closing at 109.79, and it is down 0.5% in 2023.

Canadian Cannabis LP Tier 3 Index

Tier 3 index rose 26.1% in January, and it gained again in February, rising 8.0% to 24.04. It ended at 17.66 in 2022, declining 62.8% for the year, and it has gained 36.1% so far in 2023.

New Cannabis Ventures maintains seven proprietary indices designed to help investors monitor the publicly-traded cannabis stocks, including the Global Cannabis Stock Index as well as the Canadian Cannabis LP Index and its three sub-indices. The sixth index, the American Cannabis Operator Index, was launched at the end of October 2018 and tracks the leading cultivators, processors and retailers of cannabis in the United States. Afterwards, we introduced the Ancillary Cannabis Index at the end of March 2021, reflecting the increasing number of publicly-traded companies providing goods or services to cannabis operators.