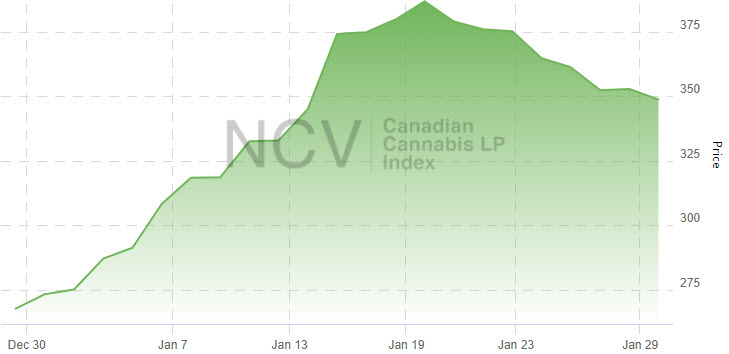

The Canadian Cannabis LP Index started 2021 strongly, advancing 26.7% to 348.75:

The index, which rallied 22.1% in Q4 but still fell 30.1% in 2020, is down 8.6% over the past year :

The index, which rallied 22.1% in Q4 but still fell 30.1% in 2020, is down 8.6% over the past year :

It remains substantially below the all-time closing high of 1314.33 in September 2018, just ahead of Canadian legalization. In March, it posted a new 52-week closing low of 196.10, a level not seen since late 2016, and it closed 77.8% above that level at the end of January:

It remains substantially below the all-time closing high of 1314.33 in September 2018, just ahead of Canadian legalization. In March, it posted a new 52-week closing low of 196.10, a level not seen since late 2016, and it closed 77.8% above that level at the end of January:

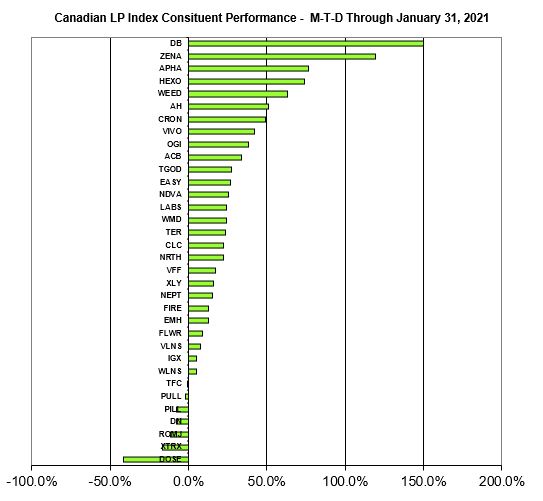

The Canadian Cannabis LP Index, which is rebalanced monthly, included 34 qualifying publicly traded licensed producers that traded in Canada at the end of December, with equal weighting for each stock. Each of the members was also included in a sub-index, with 4 in the Canadian Cannabis LP Tier 1 Index, 11 in the Canadian Cannabis LP Tier 2 Index and 19 in the Canadian Cannabis LP Tier 3 Index during the month. At the end of June, we revised the rules for inclusion, requiring companies to have a price of at least C$0.20 unless they are generating at least C$2.5 million quarterly from their cannabis production operation. Previously, we required revenue in excess of C$1 million for stocks trading below C$0.20. There are currently about two dozen publicly traded LPs that fail to qualify.

Tier 1

Tier 1, which included the LPs that are generating cannabis-related sales of at least C$25 million per quarter, soared 62% to 792.14, extending its gains since the U.S. elections in November. Tier 1 dropped 23.9% in 2020, ending the year at 488.96. We have increased the minimum revenue required to be included over time. At the beginning of 2021, we raised it from C$20 million. During 2019 and the first half of 2020, companies needed to generate revenue in excess of C$10 million for inclusion. In 2018, we used C$4 million as the hurdle.

This group included Aphria (TSX: APHA) (NASDAQ: APHA), Aurora Cannabis (TSX: ACB) (NYSE: ACB), Canopy Growth (TSX: WEED) (NASDAQ: CGC) and HEXO Corp (TSX: HEXO) (NYSE: HEXO).

Among these largest LPs by revenue, Aurora Cannabis was the worst performer, gaining 33.8%. Aphria performed the best, rising 76.7%.

Tier 2

Tier 2, which included the LPs that generate cannabis-related quarterly sales between C$5 million and C$25 million, rose 31.1% to 478.99. In 2020, it lost 35.9% in 2020, closing at 365.19. Prior to July 2020, companies needed revenue in excess of C$2.5 million to be included in this tier.

This group included Auxly (TSXV: XLY) (OTC: CBWTF), Cronos Group (TSX: CRON) (NASDAQ: CRON), Delta 9 (TSX: DN) (OTC: VNRDF), Organigram (TSX: OGI) (NASDAQ: OGI), Supreme Cannabis (TSX: FIRE) (OTC: SPRWF), TerrAscend (CSE: TER) (OTC: TRSSF), Valens Company (TSX: VLNS) (OTC: VLNCF), Village Farms (TSX: VFF) (NASDAQ: VFF), VIVO Cannabis (TSX: VIVO) (OTC: VVCIF), WeedMD (TSXV: WMD) (OTC: WDDMF) and Zenabis Global (TSX: ZENA) (OTC: ZBISF).

The worst performer was Delta 9, which declined almost 8%, while Zenabis, up 119%, was the best performer.

Tier 3

Tier 3, which included the 20 qualifying LPs that generate cannabis-related quarterly sales less than C$5 million, rose 16.8% as it closed at 77.76. It ended at 66.59 in 2020, declining 31.2%. The strongest performer was Decibel Cannabis (CSE: DBCCF), which was the best performing stock in the broader index as well.

The returns for the overall sector varied greatly, with 6 names gaining more than 50% and 3 declining by more than 10%. The entire group posted a median return of 22.6%:

For February, the overall index will have 36 constituents after the removal of Rapid Dose Therapeutics, which fell below the minimum price for companies generating less than C$2.5 million quarterly LP revenue, and the additions of Eve & Co, Namaste Technologies and Nextleaf Solutions.

For February, the overall index will have 36 constituents after the removal of Rapid Dose Therapeutics, which fell below the minimum price for companies generating less than C$2.5 million quarterly LP revenue, and the additions of Eve & Co, Namaste Technologies and Nextleaf Solutions.

In the next monthly review, we will summarize the performance for February and discuss any additions or deletions. Be sure to bookmark the pages to stay current on LP stock price movements within the day or from day-to-day.