![]()

Glass House Brands Reports Third Quarter 2022 Financial Results

- Reports record quarterly revenue of $28.3M, up 72% from Q2 2022

- Biomass production1 up 164% year-on-year and biomass revenue increased 180% year-on-year

- Record low quarterly cost per pound of $134, down 15% sequentially2

- Gross margin of 31%, increases from 2% in Q2 2022 and more than double year-earlier level

- Raised $22.5 million of new capital to date

- Q4 Revenue guidance reduced to $30–$32 million

- Target for Free Cash Flow positive operations excluding expansion capex at the SoCal Farm3 revised to Q3 2023 from Q1 2023

- Conference Call to be Held November 10, 2022 at 5:00 p.m. ET

LONG BEACH, Calif. and TORONTO, Nov. 10, 2022 /CNW/ – Glass House Brands Inc. (“Glass House” or the “Company”) (NEO: GLAS.A.U and GLAS.WT.U) (OTCQX: GLASF and GHBWF), one of the fastest-growing, vertically integrated cannabis companies in the U.S., today reported financial results for its third quarter ending September 30, 2022.

Third Quarter 2022 Highlights

(Unless otherwise stated, all results and dollar references are in U.S. dollars)

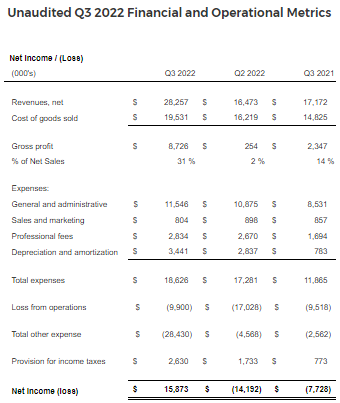

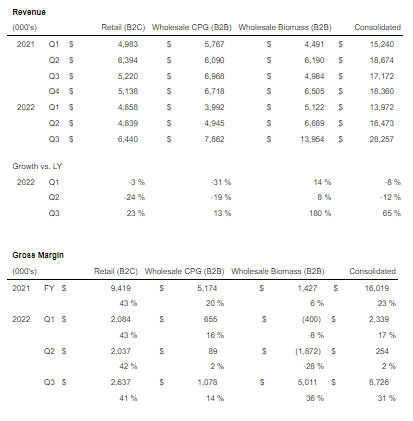

- Net Sales of $28.3 million increased 65% from $17.2 million in Q3 2021 and 72% sequentially from $16.5 million in Q2 2022.

- Gross Profit was $8.7 million compared to $2.3 million in Q3 2021 and $0.3 million in Q2 2022.

- Gross Margin was 31%, compared to 14% in Q3 2021 and 2% in Q2 2022.

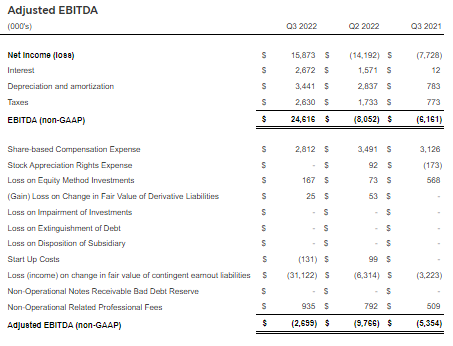

- Adjusted EBITDA4 was $(2.7) million, compared to $(5.4) million in Q3 2021 and $(9.8) million in Q2 2022.

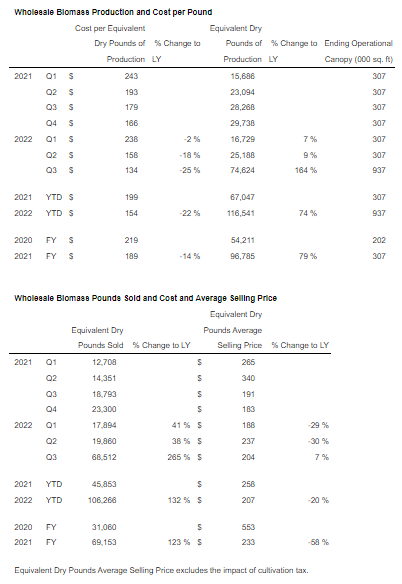

- Cost per Equivalent Dry Pound of Production1,2 was $134 a decrease of 25% compared to the same period last year and down 15% sequentially versus Q2 2022.

- Equivalent Dry Pound Production1 was 74,624 pounds, up 164% year-over-year and 196% sequentially.

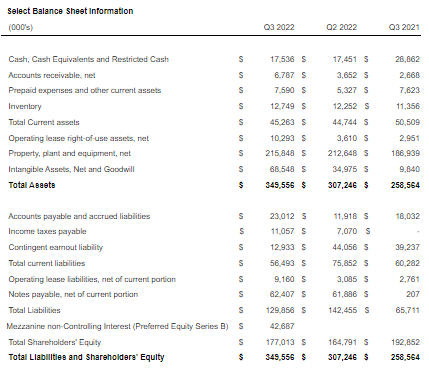

- Cash balance was $17.5 million at quarter-end, up slightly from Q2 2022 quarter end.

Management Commentary

We believe that we own and operate the best and most efficient cannabis greenhouse in the US at 5.5 million square feet in size, of which 1.5 million square feet is planted and in production.

Kyle Kazan, Co-Founder, Chairman and CEO of Glass House

Kyle Kazan, Co-Founder, Chairman and CEO of Glass House

And we are excited to show conclusive evidence that we own the unicorn of greenhouses. In the third quarter, and the first full quarter of cultivation and harvesting at the SoCal farm, we grew biomass production by 164% year-over-year and equivalent dry pounds sold by 265% to approximately 69,000 pounds.

“In just one quarter, we nearly matched the total amount of wholesale biomass we sold in all of calendar 2021, but even more remarkable is our cost structure. Despite a 21% sequential drop in cannabis flower prices, our costs fell to $134 per equivalent dry pound of production,1,2 enabling gross margin on our wholesale business to soar from 5% which excluded start-up costs in Q2 to 36% in Q3. This is precisely why we are so excited about this greenhouse; we are only operating at 20% capacity utilization of the entire farm in a market with falling sales pricing, and our gross margin is still almost 40%. Clearly we answered the 2 biggest questions we’ve heard since announcing the purchase of the massive facility, ‘Can we grow high quality cannabis cost effectively to the extreme?’ and ‘Can we sell it all?’ The answer is a resounding yes to both.”

“The competitive edge provided by our unique vertically-integrated model has never been more apparent as the cannabis industry continues to evolve. I am very proud of the work the team has done over the past quarter as their steadfast commitment continues to bring our strategic initiatives to life. We made significant progress toward our goal of being the No. 1 brand-builder in the country’s largest cannabis market including integrating the PLUS team, launching an all-new line of vegan gummies and flower under our Allswell brand and driving sequential growth in our branded CPG sales. Our retail platform, which acts as the tip of the spear for our branded products, has seen unprecedented growth as we closed transactions to fully acquire The Pottery and three Natural Healing Center Dispensaries. Since the beginning of the year, we’ve expanded our retail footprint from three locations to seven currently, with another three locations expected to open in the fourth quarter.”

“Another key development within our wholesale and branded CPG business was the signing of a new partnership with Seed Junky, one of the premier breeders in California as well as globally, to breed and select strains that will be exclusively made available in Glass House branded products including Glass House Farms, Forbidden Flowers, Field extracts and others. We’re excited to formalize and expand our relationship with Seed Junky and have great respect for the outstanding quality of the strain library that JBeezy and Wes Vazquez have built. Seed Junky Genetics is behind some of the bestselling and most widely known strains in the cannabis industry, and now Glass House will be offering new, exclusive genetics in several of its most popular product lines starting early next year. Like all of Glass House’s products, the price points of these new strains will provide an excellent value proposition. This partnership is highly complementary and should yield synergies for both companies.”

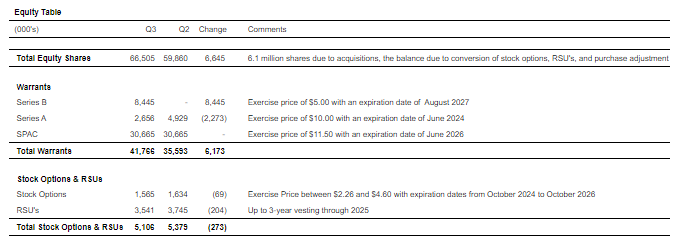

“Finally, one of the more gratifying aspects of our third quarter performance was the success of our Series B preferred equity offering (the “Offering”) in the face of extremely challenging market conditions. During the third quarter, we raised $19.5 million in new capital and facilitated the exchange of $22.7 million of existing Series A Preferred Stock for new Series B Preferred Stock. Since then, we have raised and received an additional $3 million in new capital. This is a major vote of confidence from our investors and puts us in a strong position to continue executing our strategic growth plans. The total size of the raise so far is over $45 million, making it 90% complete based on the targeted total financing amount of $50 million. We expect to complete the Offering very soon.”

Third Quarter 2022 Operational Highlights

- Glass House Brands Completes the Acquisition of the Remaining Equity Ownership in The Pottery Dispensary

- Glass House Brands Forms Genetics and Nursery Partnership with Seed Junky

- Allswell – The Value Cannabis Brand from Glass House Brands – Launches First-Ever Line of Vegan Cannabis Gummies

- Glass House Brands Closes Initial Tranche of Non-Brokered Private Placement of Equity Securities

- Glass House Brands Closes Grover Beach and Lemoore Natural Healing Center Dispensary Acquisitions

- Glass House Brands Closes Morro Bay Natural Healing Center Dispensary Acquisition

Subsequent Events

- Glass House Brands Closes Second Tranche of Non-Brokered Private Placement of Equity Securities

- Mission Green Launches New Clemency Initiative and Petitions President to Release Parker Coleman Who Is Serving 60 Years for Marijuana

- Glass House Brands Appoints Benjamin Vega as General Counsel and Corporate Secretary

Media Highlights

- Forbes Video Documentary: How America Botched Cannabis Legalization (At Minute 5)

- How the Cannabis Industry Can Begin Interstate Commerce – Legally

- High Times: Mission of Justice: The Weldon Project and Mission Green

- Seeking Alpha: Glass House’s Graham Farrar on Industry Challenges and Opportunities

- Herb.co: Allswell Believes Cannabis Should be an Affordable Right, Not a Luxury

- Best of Orange County 2022: Retail: Best Cannabis Dispensary

Q3 2022 Financial Results Discussion

Net sales for Q3 2022 were $28.3 million, 65% growth versus Q3 2021 and 72% sequential growth versus Q2 2022.

Wholesale revenue of $14.0 million increased 180% versus Q3 2021 and grew 109% sequentially versus Q2 2022. In the quarter, product sold increased 265% year-on-year to 69,000 pounds of equivalent dry weight.1 The increase in weight available for sale was driven by a 164% increase in production versus last year as a result of incremental product from the first full quarter of production of the Company’s new SoCal farm.

Retail revenue in Q3 of $6.4 million, increased by 33% sequentially and 23% year-over-year driven by incremental revenues from four recently acquired retail locations, each of which contributed revenue for only a fraction of the quarter.

Wholesale CPG revenues were $7.9 million, an increase of 59% sequentially and 13% compared to the prior year. This increase was primarily driven by the first full quarter of contribution from the PLUS edibles brand which benefited from a $900,000 initial order as we moved PLUS distribution from Nabis to Herbl at the end of August. Without the contribution of PLUS, CPG wholesale revenues were $4.7 million, up 48% sequentially and down 32% year-over-year.

Gross profit was $8.7 million, or 31% of net sales, compared to $2.3 million, or 14%, in Q3 2021 and $0.3 million, or 2% in Q2 2022. The sequential increase in gross margin was primarily due to a lower cost per equivalent dry pound of production driven by the contributions of the SoCal farm in its first full quarter of production and by markdowns returning to lower levels as a result of reduced aged CPG inventories and better inventory management.

General and administrative expenses were $11.5 million for the quarter compared to $10.9 million in Q2 2022. The $0.6 million increase is primarily attributable to increased operating expenses at the SoCal Farm related to Cannabis Taxes and the addition of the three NHC dispensaries.

Sales and marketing expenses were $0.8 million, a 10% decline compared to Q2 2022 primarily driven by the streamlining of marketing spend. Professional fees were $2.8 million, nearly consistent with Q2 2022 of $2.7 million.

Depreciation and amortization in Q3 2022 was $3.4 million compared to $2.8 million in Q2 as a result of having additional capex placed into service during the quarter.

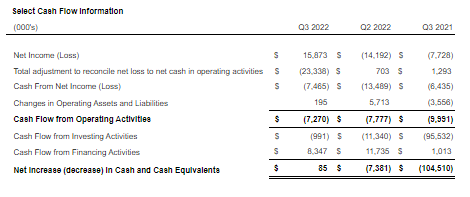

Adjusted EBITDA4 loss shrunk to $2.7 million in the third quarter, a $7.1 million improvement over a loss of $9.8 million in the second quarter of 2022. The improvement in gross margin to 31% in Q3 from 2% in Q2 resulted in a $8.5 million increase in gross profit and was the key driver of the substantial reduction in Adjusted EBITDA4 loss.

As of September 30, 2022, the Company had $17.5 million in cash, including $3 million of restricted cash, slightly up compared to Q2 2022. Cash used in operations was $7.3 million compared to $7.8 million in Q2. With the increase in revenue, the Company used about $2.4 million of working capital in cash across Accounts Payable, Accounts Receivable, Prepaids and Inventory compared to Q2 when the Company gained $4 million in cash from these same accounts. In addition, cash usage from net income decreased to $7.5 million in Q3 from $13.5 million in Q2.

Despite the positive third quarter results, there are a number of headwinds we are experiencing in the fourth quarter. As such, we are updating our previously provided Q4 2022 guidance. We now expect Q4 revenue to be in the range of $30 to $32 million from the previous projection of $50 million, reflecting reduced expectations for all three of our key business lines. In addition, due to short-term cultivation issues being experienced at our SoCal farm, we are raising the projected cost per equivalent dry pound of production to $135 per pound for Q4 from the prior guidance of $125 per pound.

A number of factors played into these revisions. Our overall business continues to be affected by challenging market conditions that have resulted in a cost-conscious consumer and a weak wholesale pricing environment. We also experienced a heat wave that saw temperatures reach 106 degrees Fahrenheit in September, which was 13 degrees higher than the highest temperature ever recorded in Camarillo. This resulted in the loss of clones in the nursery and stunted some plants in the greenhouse. We made adjustments and feel that the experience gave us important insights about our new SoCal Farm. If a similar event happened today, we are confident that we could weather it without similar output disruptions.

Taking all these factors into account, we are pushing our target for free cash flow positive operations excluding expansion capex at the SoCal Farm3 out by two quarters to the third quarter of 2023. These factors have also caused us to change our annual revenue run rate estimate to $160 million by 2023 down from $200 million. We remain confident that the incremental capital we have raised thus far, and the additional funds we intend to raise to complete our $26.5 million Offering will provide the necessary run rate to achieve this guidance.

Financial results and analyses will be available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and SEDAR (www.sedar.com).

Conference Call

The Company will host a conference call to discuss the results on today, November 10, 2022 at 5:00 p.m. Eastern Time.

Webcast: Click here

Dial-In Number: 1-888-664-6392

Conference ID: 58945425

Replay: 1-888-390-0541

Replay Code: 945425 #

(replay available until 12:00 midnight Eastern Time Thursday, November 17, 2022)

Non-GAAP Financial Measures

Glass House defines EBITDA as Net Loss (GAAP) adjusted for interest and financing costs, income taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA excluding share-based compensation, stock appreciation rights expense, loss (income) on equity method investments, change in fair value of derivative liabilities, change in fair value of contingent liabilities, acquisition related professional fees, and non-operational start-up costs.

EBITDA and Adjusted EBITDA are presented because management has evaluated the financial results both including and excluding the adjusted items and believe that the supplemental non-GAAP financial measures presented provide additional perspective and insights when analyzing the core operating performance of the business. Such supplemental non-GAAP financial measures are not standardized financial measures under U.S. GAAP used to prepare the Company’s financial statements and might not be comparable to similar financial measures disclosed by other companies and, thus, should only be considered in conjunction with the GAAP financial measures presented herein.

The Company has provided a table above that provides a reconciliation of the Company’s net loss to Adjusted EBITDA for the three months ended September 30, 2022 compared to three months ended September 30, 2021 and three months ended June 30, 2022.

Footnotes and Sources:

- Includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen not converted into dry weight by the Company.

- Cost per Equivalent Dry Pound of Production, is the application of a subset of Costs of Goods Sold for cannabis biomass production (including all expenses from nursery and cultivation to curing and trimming – the point at which product is ready for sales as wholesale cannabis or to be transferred to CPG) applied to the Company’s metric of dry production which includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen that is not converted into dry goods by the Company.

- We define free cash flow positive operations excluding expansion capex at the SoCal Farm for a given quarter as Net Cash used in Operating Activities plus Net Cash used in Investing Activities excluding capex spent for expansion at the SoCal Farm.

- EBITDA and Adjusted EBITDA are non-GAAP financial measures that are not defined by U.S. GAAP and may not be comparable to similar measures presented by other companies. Please see “Non-GAAP Financial Measures” herein for further information and for a reconciliation of such non-GAAP measures to the closest GAAP measure.

- Company has the potential to achieve monthly revenues that annualize to $160 million. The statement assumes the following in potential revenues from each source: 1) Annualized wholesale biomass sales of $60 million; 2) Annualized retail revenues of $65 million; 3) Annualized wholesale CPG revenues of $35 million.

About Glass House

Glass House is one of the fastest-growing, vertically integrated cannabis companies in the U.S., with a dedicated focus on the California market and building leading, lasting brands to serve consumers across all segments. From its greenhouse cultivation operations to its manufacturing practices, from brand-building to retailing, the company’s efforts are rooted in the respect for people, the environment, and the community that co-founders Kyle Kazan, Chairman and CEO, and Graham Farrar, President, instilled at the outset. Through its portfolio of brands, which includes Glass House Farms, Forbidden Flowers, and Mama Sue Wellness, Glass House is committed to realizing its vision of excellence: outstanding cannabis products, produced sustainably, for the benefit of all. For more information and company updates, please visit www.glasshousebrands.com and https://ir.glasshousebrands.com/contact/email-alerts/.