![]()

ScottsMiracle-Gro Announces Record First Quarter Results; U.S. Consumer Sales Increase 147%, Hawthorne Sales Rise 71%

- Company reports first-ever profit for fiscal first quarter

- Full year sales guidance increased; Non-GAAP adjusted EPS guidance reaffirmed

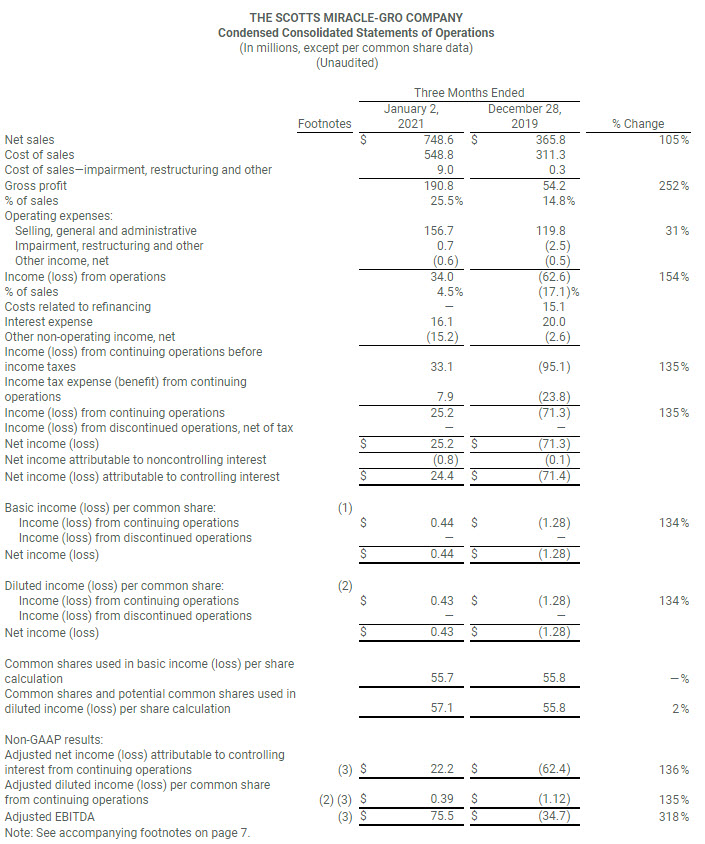

MARYSVILLE, Ohio, Feb. 03, 2021 (GLOBE NEWSWIRE) — The Scotts Miracle-Gro Company (NYSE: SMG), one of the world’s leading marketers of branded consumer lawn and garden as well as hydroponic and indoor growing products, today announced company-wide sales increased 105 percent to a record $748.6 million in its fiscal first quarter primarily driven by strong retailer support in the U.S. Consumer segment as well as continued momentum in Hawthorne.

For the quarter ended January 2, 2021, income from continuing operations was $0.43 per diluted share, compared with a loss of $1.28 per share in fiscal 2020. Non-GAAP adjusted earnings – which is the basis of the Company’s guidance – was $0.39 per diluted share in the quarter compared with a loss of $1.12 per share last year. Due to the seasonal nature of the lawn and garden category, ScottsMiracle-Gro has historically reported a loss during its first quarter. The results in 2021 mark the first time the Company has ever reported a first quarter profit.

While we anticipated a strong start to fiscal 2021, both the U.S. Consumer and Hawthorne segments surpassed our expectations and put us on a good trajectory for the balance of the year.

Jim Hagedorn, chairman and chief executive officer

Jim Hagedorn, chairman and chief executive officer

In U.S. Consumer, we are working closely with our retail partners as they prepare for the upcoming growing season. And Hawthorne continues to demonstrate its best-in-class performance within its industry, working with retailers and growers to help drive their success.

“Our strong start gives us renewed confidence in our full-year outlook although we remain sensitive to the challenges in the second half of the fiscal year against historic comparisons. We now believe we have enough visibility, however, to raise our full-year sales growth outlook for Hawthorne to a range of 20 to 30 percent, compared with our previous outlook of 15 to 20 percent. Despite the historically strong start in U.S. Consumer, it remains too early in the season to adjust our outlook for that business.”

First quarter details

For the fiscal first quarter, the Company reported sales of $748.6 million, up 105 percent from $365.8 million. Due to the Company’s fiscal calendar, the first quarter of 2021 had five more days than the first quarter of fiscal 2020. The difference had a sales impact of approximately $43 million.

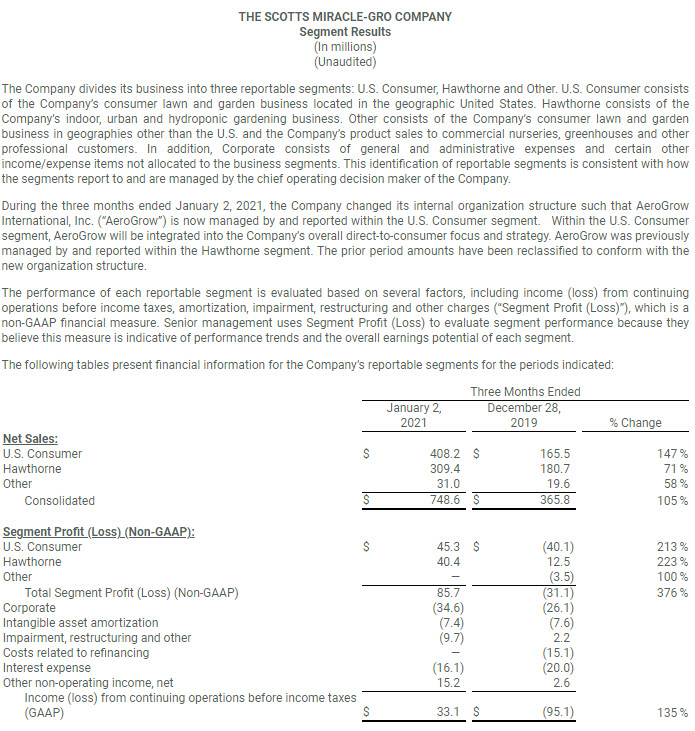

First quarter sales for the Hawthorne segment increased 71 percent to $309.4 million driven by strong demand in all categories of indoor growing equipment and supplies. U.S. Consumer segment sales increased 147 percent to $408.2 million. Consumer purchases of the Company’s products at its largest retail partners increased 40 percent in the quarter. A significant portion of the sales increase for U.S. Consumer is attributable to replenishing of retail inventory.

The company-wide GAAP and non-GAAP adjusted gross margin rates were 25.5 percent and 26.7 percent, respectively, compared with 14.8 percent and 14.9 percent a year ago. The improvement was driven by fixed cost leverage and product mix. However, some of those benefits are related to the timing of shipments and are expected to reverse in subsequent quarters.

Selling, general and administrative expenses (SG&A) increased 31 percent to $156.7 million. The increase is largely driven by increased marketing expense in the U.S. Consumer segment.

“Our investment in marketing continues to be a focus area as we strengthen our relationship with gardeners,” Hagedorn said. “Our year-round commitment to driving the conversation with consumers will include our first commercial specially produced for the Super Bowl, which is scheduled to appear in the second quarter of this Sunday’s game. That kind of reach, coupled with our data-driven and highly targeted approach to social media, is key in our efforts to retain the millions of new consumers who have entered our category over the past year.”

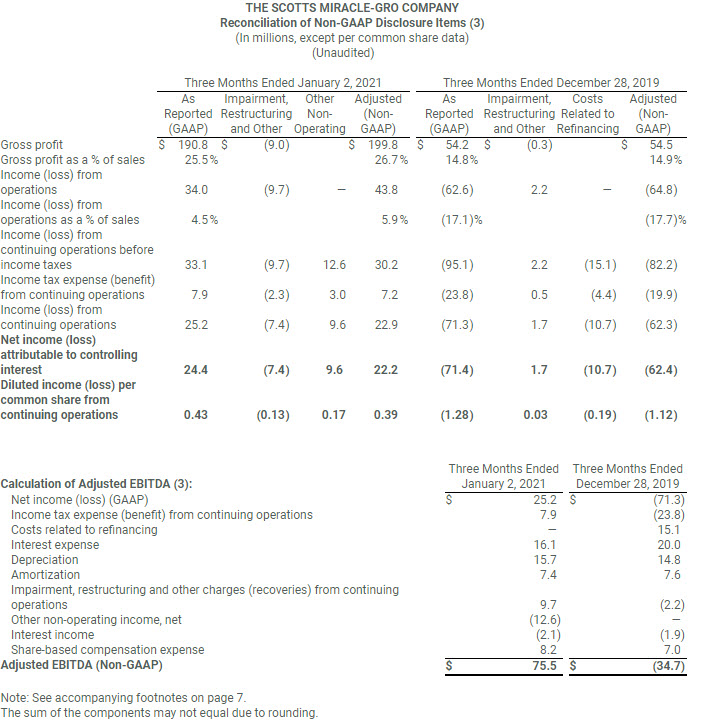

On a company-wide basis, GAAP income from continuing operations was $25.2 million, or $0.43 per share, compared with a loss of $71.3 million, or $1.28 per share, for the first quarter of fiscal 2020. Those results include impairment, restructuring and other one-time items, as well as costs related to refinancing. Excluding those items, the non-GAAP adjusted income was $22.2 million, or $0.39 per share, compared with a loss of $62.4 million, or $1.12 per share, last year.

Full-year outlook

The Company said it now expects fiscal 2021 sales growth of 1 to 6 percent compared to 0 to 5 percent previously. Hawthorne sales guidance was increased to a range of 20 to 30 percent from a previous range of 15 to 20 percent. Guidance for U.S. Consumer sales of 0 to minus 5 percent was reaffirmed. Guidance for non-GAAP adjusted EPS of $8.00 to $8.40 was reaffirmed as the Company noted that it now expects SG&A to decline 3 to 8 percent from 2020 spending levels, compared to a previous estimate of a 6 to 11 percent year-over-year decline. The adjusted gross margin rate is now expected to decline 125 to 175 basis points year-over-year due to higher commodity costs and segment mix more heavily skewed to the lower margin Hawthorne business than previously contemplated. The revised gross margin rate guidance compares to a previous expected decline of 50 basis points.

Conference Call and Webcast Scheduled for 9:00 a.m. EST Today, Feb. 3

The Company will discuss results during a webcast and conference call today at 9:00 a.m. EST. To participate in the conference call, please call 1-800-263-0877 (Conference Code: 3989033). A replay of the call can be heard by calling 1-888-203-1112. The replay will be available for 15 days. A live webcast of the call and the press release will be available on the Company’s investor relations website at http://investor.scotts.com. An archive of the press release and any accompanying information will remain available for at least a 12-month period.

About ScottsMiracle-Gro

With approximately $4.1 billion in sales, the Company is one of the world’s largest marketers of branded consumer products for lawn and garden care. The Company’s brands are among the most recognized in the industry. The Company’s Scotts®, Miracle-Gro® and Ortho® brands are market-leading in their categories. The Company’s wholly-owned subsidiary, The Hawthorne Gardening Company, is a leading provider of nutrients, lighting and other materials used in the indoor and hydroponic growing segment. For additional information, visit us at www.scottsmiraclegro.com.

THE SCOTTS MIRACLE-GRO COMPANY

Footnotes to Preceding Financial Statements

(1) Basic income (loss) per common share amounts are calculated by dividing income (loss) attributable to controlling interest from continuing operations, income (loss) from discontinued operations and net income (loss) attributable to controlling interest by the weighted average number of common shares outstanding during the period.

(2) Diluted income (loss) per common share amounts are calculated by dividing income (loss) attributable to controlling interest from continuing operations, income (loss) from discontinued operations and net income (loss) attributable to controlling interest by the weighted average number of common shares, plus all potential dilutive securities (common stock options, performance shares, performance units, restricted stock and restricted stock units) outstanding during the period.

(3) Reconciliation of Non-GAAP Measures

Use of Non-GAA

To supplement the financial measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), the Company uses non-GAA

In addition to GAA

Management believes that these non-GAA

Exclusions from Non-GAA

Non-GAA

- Impairments, which are excluded because they do not occur in or reflect the ordinary course of the Company’s ongoing business operations and their exclusion results in a metric that provides supplemental information about the sustainability of operating performance.

- Restructuring and employee severance costs, which include charges for discrete projects or transactions that fundamentally change the Company’s operations and are excluded because they are not part of the ongoing operations of its underlying business, which includes normal levels of reinvestment in the business.

- Costs related to refinancing, which are excluded because they do not typically occur in the normal course of business and may obscure analysis of trends and financial performance. Additionally, the amount and frequency of these types of charges is not consistent and is significantly impacted by the timing and size of debt financing transactions.

- Discontinued operations and other unusual items, which include costs or gains related to discrete projects or transactions and are excluded because they are not comparable from one period to the next and are not part of the ongoing operations of the Company’s underlying business.

Definitions of Non-GAA

The reconciliations of non-GAA

Adjusted gross profit: Gross profit excluding impairment, restructuring and other charges / recoveries.

Adjusted income (loss) from operations: Income (loss) from operations excluding impairment, restructuring and other charges / recoveries.

Adjusted income (loss) from continuing operations before income taxes: Income (loss) from continuing operations before income taxes excluding impairment, restructuring and other charges / recoveries and costs related to refinancing.

Adjusted income tax expense (benefit) from continuing operations: Income tax expense (benefit) from continuing operations excluding the tax effect of impairment, restructuring and other charges / recoveries and costs related to refinancing.

Adjusted income (loss) from continuing operations: Income (loss) from continuing operations excluding impairment, restructuring and other charges / recoveries and costs related to refinancing, each net of tax.

Adjusted net income (loss) attributable to controlling interest from continuing operations: Net income (loss) attributable to controlling interest excluding impairment, restructuring and other charges / recoveries, costs related to refinancing and discontinued operations, each net of tax.

Adjusted diluted income (loss) per common share from continuing operations: Diluted net income (loss) per common share from continuing operations excluding impairment, restructuring and other charges / recoveries and costs related to refinancing, each net of tax.

Adjusted EBITDA: Net income (loss) before interest, taxes, depreciation and amortization as well as certain other items such as the impact of the cumulative effect of changes in accounting, costs associated with debt refinancing and other non-recurring or non-cash items affecting net income (loss). The presentation of adjusted EBITDA is intended to be consistent with the calculation of that measure as required by the Company’s borrowing arrangements, and used to calculate a leverage ratio (maximum of 4.50 at January 2, 2021) and an interest coverage ratio (minimum of 3.00 for the twelve months ended January 2, 2021).

Free cash flow: Net cash provided by (used in) operating activities reduced by investments in property, plant and equipment.

Free cash flow productivity: Ratio of free cash flow to net income (loss).

- The World Health Organization recognized a novel strain of coronavirus (“COVID-19”) as a public health emergency of international concern on January 30, 2020 and as a global pandemic on March 11, 2020. In response to the COVID-19 pandemic, the Company has implemented additional measures intended to both protect the health and safety of its employees and maintain its ability to provide products to its customers, including (i) requiring a significant part of its workforce to work from home, (ii) monitoring its employees for COVID-19 symptoms, (iii) making additional personal protective equipment available to its operations team, (iv) requiring all manufacturing and warehousing associates to take their temperatures before beginning a shift, (v) modifying work methods and schedules of its manufacturing and field associates to create distance or add barriers between associates, consumers and others, (vi) expanding cleaning efforts at its operation centers, (vii) modifying attendance policies so that associates may elect to stay home if they have symptoms, (viii) prioritizing production for goods that are more essential to its customers and (ix) implementing an interim premium pay allowance for certain associates in its field sales force or working in manufacturing or distribution centers. During the three months ended January 2, 2021, the Company incurred costs of $8.7 million in the “Cost of sales—impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations and incurred costs of $0.6 million in the “Impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations associated with the COVID-19 pandemic primarily related to premium pay. These direct and incremental costs were excluded from the Company’s non-GAA

- On December 31, 2020, pursuant to the terms of the Contribution and Unit Purchase Agreement between the Company and Alabama Farmers Cooperative, Inc. (“AFC”), the Company acquired a 50% equity interest in the Bonnie Plants business through a newly formed joint venture with AFC (“Bonnie Plants, LLC”) in exchange for a cash payment of $100.7 million, forgiveness of the Company’s outstanding loan receivable with AFC and termination of the Company’s options to increase its economic interest in the Bonnie Plants business. The Company’s loan receivable with AFC, which was previously recognized in the “Other assets” line in the Condensed Consolidated Balance Sheets, had a carrying value of $66.4 million on December 31, 2020 and the Company recognized a gain of $12.5 million during the three months ended January 2, 2021 to write-up the value of the loan to its closing date fair value in the “Other non-operating income, net” line in the Consolidated Statements of Operations. The Company’s interest in Bonnie Plants, LLC had an initial fair value of $202.9 million and is recorded in the “Investment in unconsolidated affiliates” line in the Consolidated Balance Sheets. The Company’s interest is accounted for using the equity method of accounting, with the Company’s proportionate share of Bonnie Plants, LLC earnings subsequent to December 31, 2020 reflected in the Condensed Consolidated Statements of Operations.

For the three months ended December 28, 2019, the following items were adjusted, in accordance with the definitions above, to arrive at the non-GAAP financial measures:

- During the three months ended December 28, 2019, the Company received $2.6 million from the final settlement of escrow funds related to a previous Hawthorne acquisition that was recognized in the “Impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations.

- On October 23, 2019, the Company redeemed all of its outstanding 6.000% Senior Notes for a redemption price of $412.5 million, comprised of $0.5 million of accrued and unpaid interest, $12.0 million of redemption premium, and $400.0 million for outstanding principal amount. The $12.0 million redemption premium was recognized in the “Costs related to refinancing” line on the Condensed Consolidated Statements of Operations during the three months ended December 28, 2019. Additionally, the Company had $3.1 million in unamortized bond issuance costs associated with the 6.000% Senior Notes, which were written-off during the three months ended December 28, 2019 and were recognized in the “Costs related to refinancing” line in the Condensed Consolidated Statements of Operations.