![]()

This news release constitutes a “designated news release” for the purposes of the Company’s prospectus supplement dated May 2, 2022 to its short form base shelf prospectus dated May 7, 2021 and amended and restated on May 25, 2021.

- Strategic realignment demonstrates significant results across the business, including quarter over quarter improvements to Adjusted EBITDA and increased gross margin before adjustments

- HEXO has signed new cultivation agreements and purged unprofitable sales

- Redecan brand achieved record sales, prompting 300% increase in production

GATINEAU, Quebec, Dec. 15, 2022 (GLOBE NEWSWIRE) — HEXO Corp. (TSX: HEXO; NASDAQ: HEXO) (“HEXO” or the “Company”), a leading producer of high-quality cannabis products, today reported its financial results for the first quarter (“Q1’23”). All currency amounts are stated in Canadian dollars unless otherwise noted.

The first quarter of 2023 has been one of incredible progress for HEXO. We’re now seeing the results of the strategic realignment we executed over the past two quarters and have successfully reset the Company for long-term success.

Charlie Bowman, President and CEO of HEXO

Charlie Bowman, President and CEO of HEXO

Our laser focus on tackling the balance sheet, pulling back on those unprofitable products where our strengths in premium cultivation were not being leveraged and expanding further into opportunities where we know we can win, is paying off across the business.

“Over the past six months, we’ve made favourable amendments to our debt structure and have paid off, in early December, more than $40 million of legacy debt. We’ve reduced our general and administrative and selling, marketing and promotion expenses by $18 million and have substantially lowered our overhead costs,” noted Julius Ivancsits, Chief Financial Officer of HEXO. “We’ve increased our gross profit before fair value adjustments by approximately $41 million over the previous quarter and have significantly decreased our inventory levels. We’ve also eliminated unprofitable sales, redeploying those resources into profitable business segments.”

“These actions have paved the way for profitable growth and we’re now building positions of strength in those areas where HEXO excels,” continued Mr. Bowman. “We’ve redesigned and upgraded our Masson grow facility, have signed new cultivation agreements, including the partnerships with Entourage and Tilray, and have announced the launch of a top shelf, premium brand, T 2.0, into the Canadian marketplace. Our Redecan brand achieved record sales in the quarter and we’ve since increased our output of Redees pre-rolls by more than 300% with no capital investment, enabling us to expand our portfolio to meet consumer demand across Canada for these products.”

Significant Financial Results

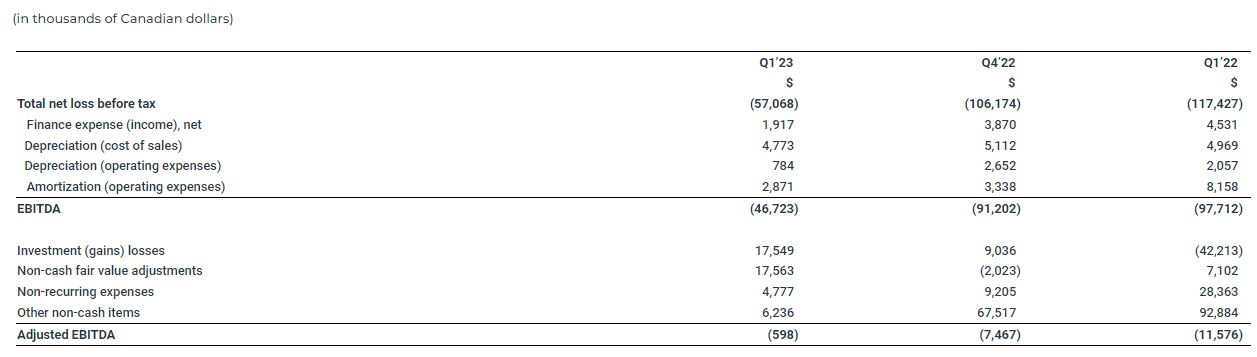

- The Company recorded an Adjusted EBITDA loss of $(0.6) million during the three months ended October 31, 2022 (“Q1’23”), an improvement of $6.9 million from the fourth quarter of FY22 (“Q4’22”), and an improvement of $11 million from the first quarter of FY22 (“Q1’22”).

- The Company recorded a total net loss before tax of $(57.1) million in Q1’23, an improvement as compared to net losses before tax of $(106.2) million in Q4’22 and $(117.4) million in Q1’22, respectively.

- Q1’23 net revenues were $35.8 million, a decrease of 29% comparatively to $50.2 million in Q1’22 and a decrease of 16% compared to $42.5 million net revenue in Q4’22.

- Total operating expenses were significantly reduced by 69% or $50.7 million quarter over quarter and 81% or $100 million as compared to Q1’22.

- Operating cash outflows were reduced by $27.7 million or 49% when compared to Q1’22.

Key Financial Results

Net Revenue:

- Q1’23 total net revenue decreased by 16% compared to Q4’22. The decline was in part, attributable to the timing of revenue recognition as certain shipments failed to reach their destination due to severe weather towards the period end. Other challenges were faced, leading to shortages of desired products, and short filling purchase orders as the Company continues to implement its revised demand planning process.

- Q1’23 total net revenue decreased by 29% compared to Q1’22. The decline in revenue is attributable to proactive decisions to realign the HEXO brand’s profitable product and cull products that were no longer meeting profitability standards.

Cost of Goods Sold & Adjusted Gross Margin:

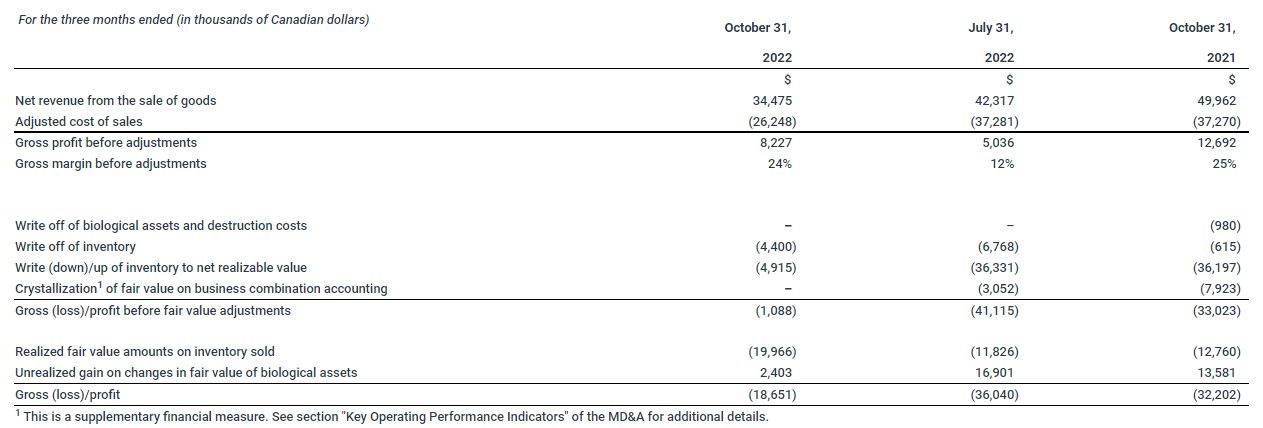

The following table summarizes and reconciles the Company’s gross profit line items per IFRS to the Company’s selected non-IFRS financial measures adjusted cost of sales, gross profit/margin before adjustments and gross profit before fair value adjustments. Refer to the ‘Non-IFRS Measures’ section below for definitions.

- Total gross margin before adjustments has been improved to 24% from 12% quarter over quarter, in part as a result of certain inefficiencies recognized in Q4’22 due to the consolidation of operations and facility closure.

- Cost of goods sold improved to $35.6 million in Q1’23 relative to $83.0 million recognized in Q1’22 and $83.4 million in Q4’22. Driving the improvements were the significant reductions to inventory impairments and net realizable value adjustments as management continues to focus on aligning cultivation to demand and mitigate the risk of aged out and unsellable stock. Additionally, the crystallization of fair value from business combinations was fully realized in Q4’22 and therefore did not factor into Q1’23.

- Unrealized gains on changes in fair value of biological assets has significantly declined primarily as the result of fewer plants on hand. The Company harvested the bulk of its outdoor grow cultivated over the summer months during the period and relative to Q1’22 the Company has reduced its total grow facilities through the consolidation and reorganization of its operational footprint.

Operating Expenses

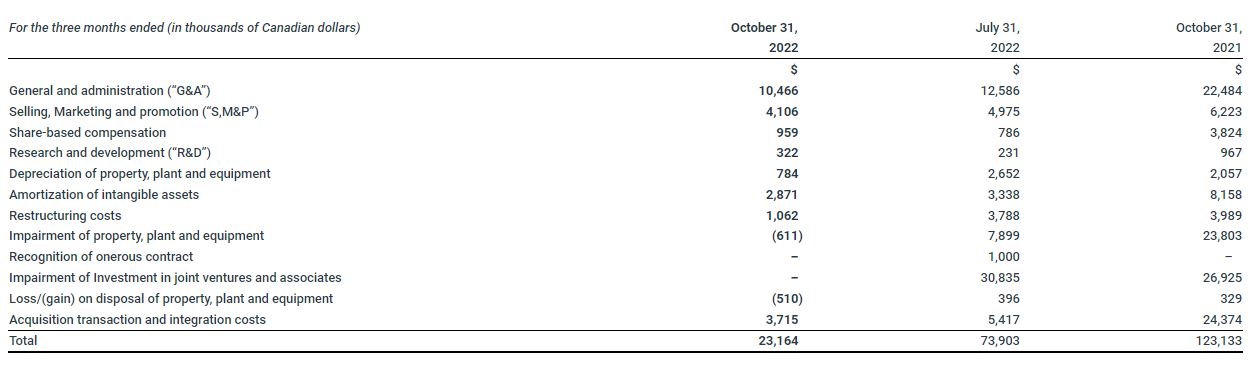

General and Administration Expenses by Nature

Operating Expenses:

- Operating expenses in Q1’23 totaled $23.2 million, a $50.7 million improvement from Q4’22. Excluding the impact of impairments and restructuring activities, operating expenses have decreased $17.2 million as a result of the Company’s cost saving measures and reduced sunk costs and overhead charges from the Zenabis deconsolidation in Q4’22.

- Operating expenses in Q1’23 decreased by $100 million or 81% comparatively from Q1’22. Driving the improvements was the significant reduction in acquisition, transaction and integration charges from the Company’s M&A activity in Q1’22 as well as the reduction to non-cash impairment losses. However, the Company’s G&A, S,M&P and R&D operating expenses have decreased $14.8 million relative to Q1’22 due to general cost saving measures, realized efficiencies, reorganization of the business structure and the restructuring of these consolidated operations.

Other income and losses

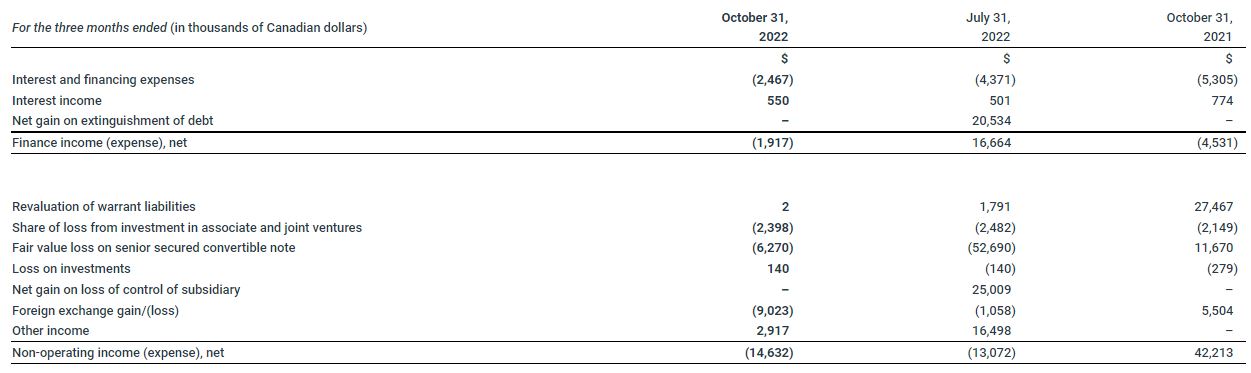

- Total non-operating expenses and finance expenses decreased $20.1 million quarter over quarter. The extinguishment of debt, the fully amortization of the day 1 loss associated with previous senior secured note and loss of control of the Zenabis Group were Q4’22 specific events which had no impact on the current period. Other income has decreased sequentially due to the net gain realized on the Belleville lease termination, another Q4’22 specific event. Unrealized foreign exchange losses were the result of unfavorable CAD/USD rates applied to the Company’s USD denominated debt.

- Total non-operating expenses and finance expenses decreased $54.2 million relative to Q1’22. Driving this change were the reduced volatility in the revaluation of warrants, a favorable fair valuation gain on the previous senior secured convertible note, and foreign exchange gains due to favorable CAD/USD rates.

Reconciliation of Adjusted Earnings before interests, taxes, depreciation and amortization (“EBITDA”) to Total net loss before tax

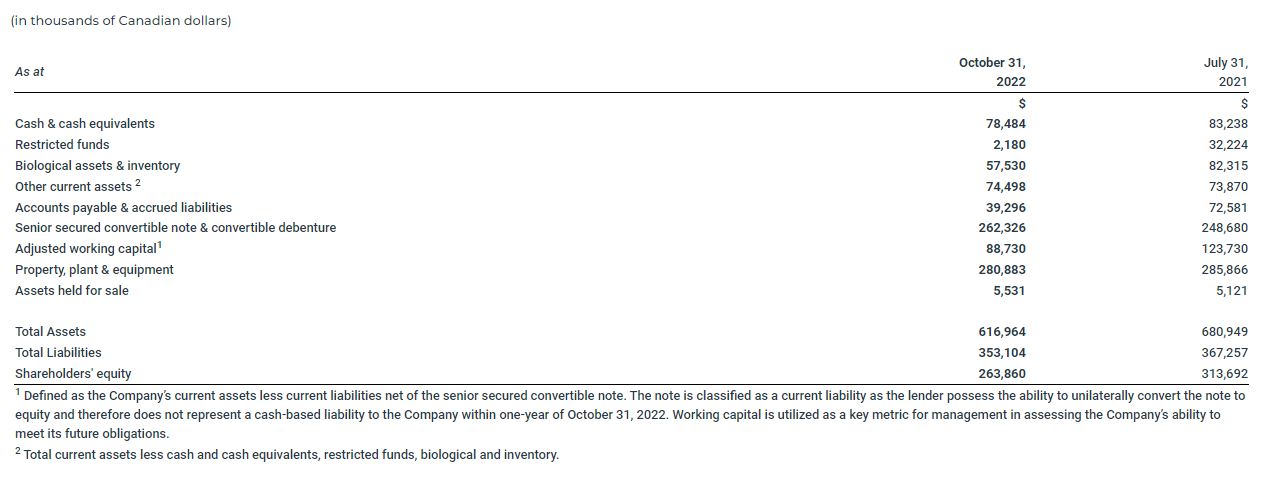

Select Balance Sheet Metrics

Liquidity Risk

The Company’s ability to continue as a going concern is dependent upon its ability in the future to achieve profitable operations and, in the meantime, to obtain the necessary financing to meet its obligations and comply with the related covenants, and to repay its liabilities when they become due. External financing, predominantly by the issuance of equity to the public or debt, will be sought to finance the operations of the Company.

On October 31, 2022, the Company had cash and cash equivalents of $78.5 million ($83.2 million at July 31, 2022). Subsequent to Q1’23 on December 5, 2022, the Company’s 8% convertible debenture matured and a total of $40.7 million was repaid in respect of the outstanding principal and unpaid interest. Under the terms of the senior secured convertible note, the Company is subject to a minimum liquidity covenant of US$20 million.

Thus, there remains a risk that the Company’s cost saving initiatives may not yield sufficient operating cash flow to meet its financial covenant requirements, and as such, these circumstances create material uncertainties that lend substantial doubt as to the ability of the Company to meet its obligations as they come due and, accordingly, the appropriateness of the use of accounting principles applicable to a going concern.

About HEXO Corp.

HEXO is an award-winning licensed producer of innovative products for the global cannabis market. HEXO serves the Canadian recreational market with a brand portfolio including HEXO, Redecan, UP Cannabis, Original Stash, 48North, Trail Mix, Bake Sale and Latitude brands, and the medical market in Canada. With the completion of HEXO’s acquisitions of Redecan and 48North, HEXO is a leading cannabis products company in Canada by recreational market share. For more information, please visit hexocorp.com.

Non-IFRS Measures

In this press release, reference is made to adjusted cost of sales, gross profit before adjustment, profit/margin before fair value adjustments, adjusted gross profit/margin, adjusted EBITDA, crystallization and adjusted working capital which are not measures of financial performance under International Financial Reporting Standards (IFRS). These metrics and measures are not recognized measures under IFRS, do not have meanings prescribed under IFRS, and are unlikely to be comparable to similar measures presented by other companies. These measures are provided as information complementary to those IFRS measures by providing a further understanding of our operating results from the perspective of management. As such, these measures should not be considered in isolation or in lieu of a review of our financial information reported under IFRS. Definitions and reconciliations for all terms above can be found in the Company’s Management’s Discussion and Analysis for the quarter ended October 31, 2022, filed under the Company’s profile on SEDAR at www.sedar.com and EDGAR at www.sec.gov respectively.