![]()

HEXO Reports Q4’22 and FY22 Financial Results

Organizational reset strengthened the business and has positioned HEXO for long-term success

This news release constitutes a “designated news release” for the purposes of the Company’s prospectus supplement dated May 2, 2022 to its short form base shelf prospectus dated May 7, 2021 and amended and restated on May 25, 2021.

GATINEAU, Québec, Oct. 31, 2022 (GLOBE NEWSWIRE) — HEXO Corp. (TSX: HEXO; NASDAQ: HEXO) (“HEXO” or the “Company”), a leading producer of high-quality cannabis products, today reported its financial results for the fourth quarter (“Q4’22”) and fiscal year ended July 31, 2022 (“FY22”). All currency amounts are stated in Canadian thousands unless otherwise noted.

“The fourth quarter was a period of strategic realignment for HEXO,” said Charlie Bowman, President and CEO of HEXO. “We focused on making the changes that will enable HEXO to maintain and expand our strong position within the Canadian cannabis market. By committing to three key priorities – aligning the Company for success, resetting the organization for profit and growth, and delivering a preferred cannabis experience for its customers and other stakeholders – we took the necessary steps to position the Company for long-term success and have come out stronger as a business.”

“Re-financing of the senior secured convertible note deleverage the balance sheet and boosted cash reserves, allowing us to focus on profitable growth,” said Julius Ivancsits, Acting Chief Financial Officer of HEXO. “We are hyper-focused on cash flow, and to this end, reduced our personnel cost by $65M, divested from businesses that do not offer HEXO a competitive advantage and focused on our quality of earnings, while also optimizing our working capital. We also rationalized to upgrade our product mix.”

With a solid foundation now in place, HEXO has moved to the second phase of our transformation – focusing on producing the core brands and products that customers want, leading in innovation and reinforcing our market share.

Charlie Bowman, President and CEO of HEXO

Charlie Bowman, President and CEO of HEXO

We evolved our leadership across the organization and are benefiting from strong integration across our most successful brands. By concentrating on these products and ensuring that they do not compete against each other, we have built a loyal customer following and refined what truly sets HEXO apart from our peers.

Significant Financial Results

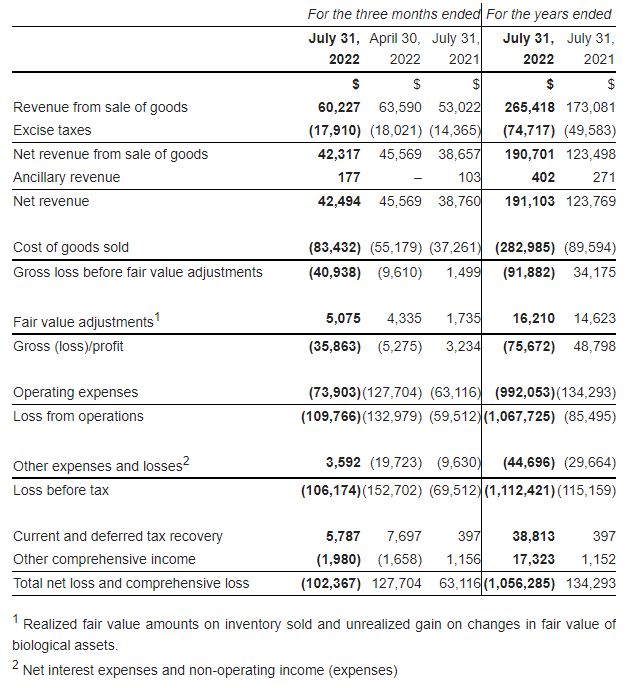

- HEXO recorded net revenue in FY22 of $191.1 million, up from $123.8 million from the fiscal year ended July 31, 2021 (“FY21”).

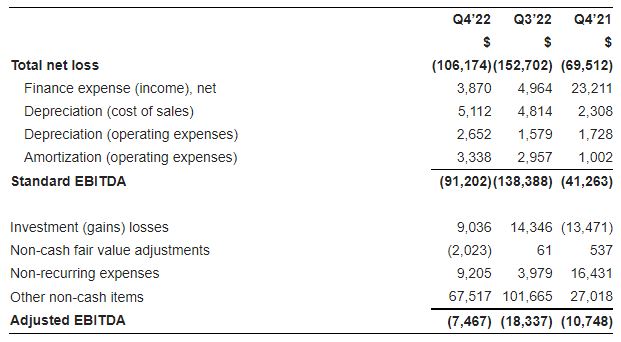

- The Company recorded an Adjusted EBITDA loss of ($7,467) in Q4’22, an improvement of $10,870, from Q3’22, and an improvement of $3,281 from the fourth quarter of FY21 (“Q4’21”).

- HEXO closed the Tilray transaction, amending the terms of the Senior Secured Convertible Notes and reducing the associated liquidity and dilution pressures under the previous debt structure.

- HEXO recorded Q4’22 net revenue of $42.5 million, an increase of 10% compared to $38.8 million in Q4’21 and a decrease of 7% compared to $45.6 million net revenue in the third quarter of FY22 (“Q3’22”).

- Q4’22 general, administrative, R&D, selling, marketing and promotion costs as percentage of net sales improved by 43% and 32%, relative to Q3’22 and Q4’21 respectively. This key ratio remained flat FY22 vs. FY21, however the Company’s size and scope increased significantly upon the acquisition of Redecan in the first quarter of FY22 (“Q1’22”).

- Total operating expenses reduced by 42%, quarter over quarter.

Significant Events

Amended Senior Secured Convertible Note

On July 12, 2022, the Company, Tilray Brands Inc. (“Tilray”) and HT Investments MA LLC (“HTI”) amended and restated the terms of the outstanding senior secured convertible note originally issued by the Company to HTI (the “Original Note”). The amended and restated convertible note (the “A&R Note”) was immediately assigned to Tilray pursuant to the terms of an amended and restated assignment and assumption agreement. Tilray acquired 100% of the remaining outstanding principal balance of US$173.7 million of the A&R Note.

The Original Note originally allowed the holder to require the Company to partially redeem the Original Note under certain conditions. The holder’s optional redemption payments mechanism has been removed from the A&R Note, which eliminates the previous risk of forced monthly redemption payments, payable in cash, when the Company did not satisfy the equity condition defined in the agreement. Management was not able to elect satisfying the Optional Redemptions through the issuance of equity. The amended salient terms under the A&R Note include a three-year extension of the maturity date to May 1, 2026, adding semiannual interest payments at 5%, removal of the 9.99% ownership limitation and unrestricting cash of US$85.7 million.

Zenabis CCAA Filing and loss of control

On June 17, 2022, Zenabis Global Inc. (“Zenabis”) and its direct and indirect wholly-owned subsidiaries (collectively, the “Zenabis Group”) filed a petition with the Superior Court of Québec for protection under the Companies’ Creditors Arrangement Act (the “CCAA”) in order to restructure their business and financial affairs. Upon filing for CCAA, management determined that control of Zenabis was lost due to the cessation of management’s ability to have the power to direct the relevant activities of Zenabis.

Following the deconsolidation, the carrying value of assets and liabilities of Zenabis were removed from the Company’s consolidated statements of financial position. The total amount deconsolidated from HEXO’s balance sheet was $82 million, including $3.4 million of cash, $29.6 million of inventory and biological assets, $13.8 million of property, plant and equipment and assets held for sale, $55.5 million of secured debenture and ($21.0) million of other assets and liabilities, net. The Company recognized a gain on derecognition of the net assets of Zenabis in non-operating income totalling $25.0 million.

The Company was informed that, on October 31, 2022, a subsidiary of SNDL Inc. acquired certain assets and shares of the members of the Zenabis Group and, as of such date, the Company no longer has any direct or indirect shareholdings in or corporate affiliation with the Zenabis Group.

Liquidity Risk

As stated above, during Q4’22, management recapitalized the Company’s senior debt and significantly improved its liquidity position and working capital. Concurrent with the debt restructuring, in Q3’22 the Company entered into a definitive agreement with an affiliate of KAOS Capital Ltd (“KAOS”), to provide a $180 million equity purchase agreement (the “ELOC”), which could provide the Company access to $5 million capital per month over a 36-month period in order to help ensure debt and interest repayments under the amended and reassigned secured note can be met. The common shares to be issued under the ELOC (the “ELOC Shares”) will be issued at a 7% discount to the 20-day volume weighted average price of the common shares on the Toronto Stock Exchange at the time the demand is made. The Company intends to utilize 60% of the acquired proceeds towards the debt and interest payments associated with the Convertible note payable. As of the date of this press release, the prospectus supplement qualifying the ELOC Shares had not been filed and the ELOC had therefore not been drawn upon.

During the latter half of the fiscal year, the Company’s new management identified and commenced certain opportunities and cost savings initiatives to fundamentally realign the operating expenses and cashflows to drive profitability and address the liquidity issues. These initiatives include:

- Entering into commercial agreements with Tilray including (i) a co-manufacturing agreement providing for manufacturing services between the parties, (ii) an advisory services agreement for certain advisory services to be provided by Tilray to HEXO, and (iii) a procurement and cost-savings agreement for efficiencies to be achieved in each party’s business with respect to administrative services, third-party commercial services, procurement, internal distribution services on an ongoing basis through creation of an Efficiencies Committee with joint representation from HEXO and Tilray, and agreeing with Tilray to negotiate an agreement concerning international sales and supply arrangements.

- Reducing of the Company’s total headcount and restructuring the organization for expected future operating and administrative needs;

- Minimizing the Company’s reliance on third party service providers and reducing professional fees; and

- Liquidating some of the Company’s previously announced decommissioned and available for sale assets.

On July 31, 2022, the Company held cash and cash equivalents of $83,238 ($67,462 at July 31, 2021) which management determines to be sufficient to meet the Company’s expected working capital and operating cash flow needs over the next 12 months, however, the Company remains subject to a minimum liquidity covenant of US$20 million under the Convertible note payable as well as certain financial and non-financial covenants. Furthermore, the Company’s 8% convertible debenture matures in December 2022, which will require a cash repayment of $40,140.

There remains a risk that the Company’s cost saving initiatives may not yield sufficient operating cash flow to meet its financial covenant requirements, and as such, these circumstances create material uncertainties that lend substantial doubt as to the ability of the Company to meet its obligations as they come due and, accordingly, the appropriateness of the use of accounting principles applicable to a going concern.

Key Financial Results

Operating Expenses

- Net revenues:

- Q4’22 net revenues have increased by 10% over Q4’21 net revenues as the result of the accretive sales contributed by the acquisition of Redecan (acquired Q1’22), which contributed net revenue of $18,274 in Q4’22. Excluding the impact of business acquisitions, net revenues have declined by 38%, driven by declines in sales of exited brands and sku rationalization.

- FY22 revenues totaled $191,103, representing a 54% increase when compared to FY21. This increase is mainly attributable to the acquisitions of Redecan (acquired Q1’22) and Zenabis (acquired Q4’21), which contributed $60,297 and $30,816 of net revenue in FY22, respectively. Excluding the impact of business acquisitions, net revenues have declined by 19%.

- Cost of Sales & Adjusted Gross Margin:

- Total Q4’22 non-beverage related adjusted gross margins decreased to 14% from 25% when compared to Q4’21 as the result of a lower average price per gram and unfavorable production variances.

- Inventory write offs, destruction, and adjustments to net realizable value totaled $43,099 in Q4’22 primarily due to aged out and excess stock.

- Crystallization of fair value from business combinations amounted to $3,052 compared to $2,272 in Q4’21.

- Operating Expenses:

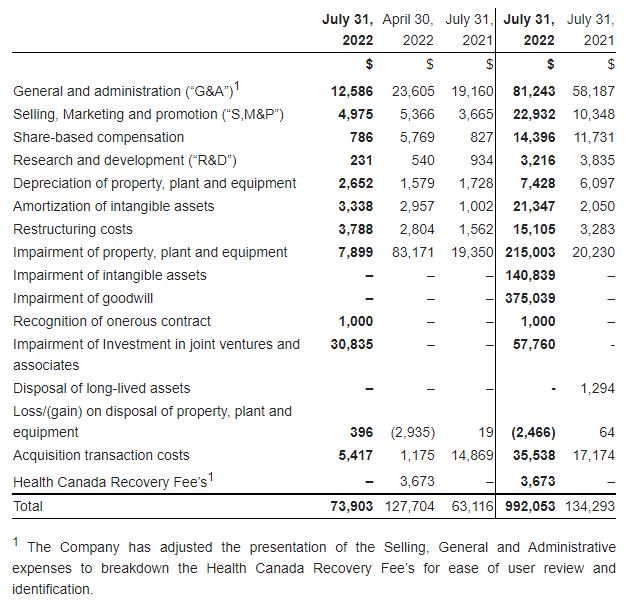

- Operating expenses in Q4’22 totaled $73,903, a 17% increase from Q4’21. The main driver for the increase is the non-cash impairment loss of the Company’s investment in Truss LP. Excluding that the Truss impairment, operating expenses have decreased by 32% relative to Q4’21 as a result of the Company’s cost saving measures.

- On an annual basis, operating expenses have increased from $134,293 in FY’21 to $992,053 in FY22. The majority of this difference is attributable to non-cash impairments in the Company’s fixed and intangible assets, as well as the Q2’22 impairment of the Company’s goodwill from acquisitions.

- G&A and S,M&P expenses increased as the general scale of the Company’s operations increased due to business acquisitions in Q4’21 and Q1’22, resulting in higher SG&A expenses.

- The Company’s restructuring activities totaled $15,105 during FY22 to align operations towards the path to profitability.

- Excluding impairments and restructuring costs, operating expenses have increased by 70%, mainly attributable to increased acquisition costs related to Redecan and 48North, the costs of recapitalizing the Company’s Convertible note payable, and increased amortization in FY22 due to the Company’s acquired intangible assets on business acquisitions.

- Other Income and Losses:

- The Q4’22 finance income (expense) totaled $16,664, compared to $(23,212) Q4’21. The main drivers of the Q4’22 amount are the $20,534 net gain on extinguishment of debt related to the Convertible note payable, while the Q4’21 balance is driven by $18.8 million in financing fees related to The Original Note and $3.0 million of interest expense from the acquired debt of Zenabis.

- The FY’22 finance income (expense) of $2,112 is driven by interest payments on the company’s senior convertible notes, which was largely offset by the net gain on the extinguishment related to the A&R Note. The FY’21 balance of $(30,523) was driven by financing fees related Original Note and Zenabis acquisition Q4’21 mentioned above and additional interest expense on the Company’s convertible debentures.

- The Q4’22 Non-operating income (expense) totaled $(13,072). The main drivers of the balance are the amortized Day 1 loss on the A&R Note, the net gain on loss of control of subsidiary, and the gain on the Belleville lease termination.

- The FY22 non-operating income (expense) totaled $(46,808), with the main drivers being the amortized Day 1 loss on the A&R Note, the revaluation gain on the company’s financial instruments, the net gain on loss of control of subsidiary, and the gain on the Belleville lease termination.

- Non-operating income (expense) for FY21 totaled $859, with the main drivers being the amortized day 1 loss on the A&R Note, revaluation losses on the Company’s financial instruments, and losses from investments in joint ventures. These amounts are largely offset by foreign exchange gains from the Company’s USD cash balances and recognized recoveries on partnerships in connection to Truss LP.

Select Balance Sheet Metrics

Adjusted EBITDA

Quarter over quarter the Company’s Adjusted EBITDA improved by $10,870. This was driven by the Company’s 39% total cost savings in general, administrative, marketing and promotion expense. The improvements are the result of the restructuring efforts and rightsizing of its operations and headcount (payroll expenses). The Company notes that the impact of the $3,673 Health Canada cannabis fee (a 2.3% levy based upon the Company’s total cannabis sales from the period of April 1, 2021 to March 31, 2022, net of shipping and purchased cannabis costs) is recognized in the third quarter each fiscal year. The Company’s G&A, R&D and S,M&P operating expenses as a percentage of net sales in Q4’22 was improved by 20% from the previous quarter. Offsetting the above improvements to Adjusted EBITDA is the lower adjusted gross margin recognized in the period.

Auditor Resignation

On October 11, 2022, the Company’s auditor, PricewaterhouseCoopers LLP (“PwC”), notified the Company of its decision, at its own initiative, to decline to stand for re-appointment as the Company’s auditor following the issuance of its auditor’s report on the Company’s consolidated financial statements for the financial year ending July 31, 2022. In accordance with the requirements of National Instrument 51-102 – Continuous Disclosure Obligations (“NI 51-102″), a change of auditor notice and PwC’s acknowledgment letter have been filed under HEXO’s profile on SEDAR. There were no “reportable events” (within the meaning of NI 51-102) involving PwC.

Non-IFRS Measures

In this press release, reference is made to gross profit before adjustment, profit/margin before fair value adjustments, adjusted gross profit/margin, adjusted EBITDA, and adjusted working capital which are not measures of financial performance under International Financial Reporting Standards (IFRS). These metrics and measures are not recognized measures under IFRS, do not have meanings prescribed under IFRS, and are unlikely to be comparable to similar measures presented by other companies. These measures are provided as information complementary to those IFRS measures by providing a further understanding of our operating results from the perspective of management. As such, these measures should not be considered in isolation or in lieu of a review of our financial information reported under IFRS. Definitions and reconciliations for all terms above can be found in the Company’s Management’s Discussion and Analysis for the fiscal year ended July 31, 2022, filed under the Company’s profile on SEDAR at www.sedar.com and EDGAR at www.sec.gov respectively.

About HEXO Corp.

HEXO is an award-winning licensed producer of innovative products for the global cannabis market. HEXO serves the Canadian recreational market with a brand portfolio including HEXO, Redecan, UP Cannabis, Original Stash, 48North, Trail Mix, Bake Sale and Latitude brands, and the medical market in Canada and Israel. The Company also serves the Colorado market through its Powered by HEXO® strategy and Truss CBD USA, a joint venture with Molson-Coors. With the completion of HEXO’s acquisitions of Redecan and 48North, HEXO is a leading cannabis products company in Canada by recreational market share. For more information, please visit hexocorp.com.