In September, Health Canada updated market information that showed how oils are growing rapidly. During the quarter ending 6/30, licensed producers (LPs) shipped 5.896mm grams of dried flower, representing growth of just 1% from the prior quarter and 46% from a year ago. Oil sales, expressed in weight, were 6.194mm grams, up 9% from the prior quarter and 313% from a year ago.

Not all LPs are positioned to capitalize on this trend, with many not yet permitted to sell oils. Among the bigger LPs, all are now selling, but the popularity of oils has benefited some more than others. With that in mind, I wanted to compare each of the major LPs, including Aphria, Aurora Cannabis, CanniMed Therapeutics, CannTrust, Canopy Growth and MedReleaf.

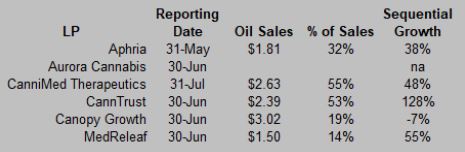

Aphria (TSX: APH) (OTC: APHQF) reported its results for the fiscal year ending in May in July. For Q4, it reported that oils represented 31.7% of sales, or about C$1.81mm. In Q3, oils represented 25.6% of sales, or C$1.31mm, suggesting that the 38% sequential growth accounted for 83% of the increase in Aphria’s Q4 sales compared to Q3. The company held inventory of 1091 liters of oil valued at C$682K on May 31.

Aurora Cannabis (TSX: ACB) (OTC: ACBFF), which launched its oils in April, reported its results for the fiscal year ending in June in September. Unfortunately, it didn’t break out the sales. The company suggested at the end of August that sales for the month would exceed C$3mm, with oils representing approximately 26% of sales.

CanniMed Therapeutics (TSX: CMED) (OTC: CMMDF) reported its FY17-Q3 ending in July in mid-September. Oils represented approximately 55% of sales, or C$2.63mm. In the prior quarter, sales of C$1.78mm represented 48% of sales. Oil sales accounted for 78.6% of the growth in Q3 sales over Q2’s. The company sold 1114 liters during Q3, an increase of 208% from a year ago, while dried cannabis grams rose by 42%.

CannTrust (CSE: TRST) (OTC: CNTTF) reported its Q2 ending in June at the end of August. Oil sales, at C$2.39mm, represented almost 53% of overall sales and increased from C$1.05mm in the prior quarter, driving 89% of the overall quarterly increase. CannTrust first sold oils in August 2016.

Canopy Growth (TSX: WEED) (OTC: TWMJF) reported its FY18-Q1 ending in June in mid-August. The company’s oil sales were 19% of revenue, or approximately C$3.02mm. The proportion of oil sales, which dropped about 7%, fell slightly from 22% in Q4 (C$3.23mm) but was up from 6% in FY17-Q1. The company has recently brought online a massive extractor made by Advanced Extraction Systems and reported 6.5mm grams of dried cannabis awaiting conversion and 2683 liters of oil in inventory.

MedReleaf (TSX: LEAF) (OTC: MEDFF) reported its FY18-Q1 ending in June in mid-August. It began selling oils in November 2016. Sales of C$1.50mm represented just 14.4% of sales, up from C$967K in the prior quarter, or 9.3%, helping to offset a decline in sales from dried cannabis. The company disclosed that oil represented 23% of overall June sales and that it expects to get to 50% of overall sales over the next several quarters.

Oils are contributing to the growth of the leading LPs in Canada, and the producers are all well positioned to benefit over the next year and beyond as medical cannabis patients adopt these products over dried flower. How oils fit into legal cannabis sales is a topic for future discussion, as the types on non-flower products that are so popular in the black market and in the United States, including edibles and extracts with higher potency and different form factors (like shatters and waxes), are not yet permitted in Canada. Further, success in the current form of extracts doesn’t suggest that the LP will be able to successfully create and market the products and brands that the consumer market will desire.