Innovative Industrial Properties Reports Fourth Quarter and Full-Year 2020 Results

Acquisitions and Portfolio Performance Drive FY 2020 Y-o-Y Growth of 162% in Total Revenues, 191% in Net Income and 180% in AFFO

SAN DIEGO, February 24, 2021–(BUSINESS WIRE)–Innovative Industrial Properties, Inc. (IIP), the first and only real estate company on the New York Stock Exchange (NYSE: IIPR) focused on the regulated U.S. cannabis industry, announced today results for the fourth quarter and year ended December 31, 2020, the fourth full year since IIP commenced real estate operations and completed its initial public offering in December 2016.

Full Year 2020 Highlights

- Generated total revenues of approximately $116.9 million, net income attributable to common stockholders of approximately $64.4 million and adjusted funds from operations (“AFFO”) of approximately $97.8 million, representing increases of 162%, 191% and 180% over 2019, respectively.

- Recorded $3.27 of net income attributable to common stockholders per diluted share and $5.00 of adjusted funds from operations (“AFFO”) per diluted share, representing increases of 61% and 53% over 2019, respectively.

- Declared dividends to common stockholders totaling $4.47 per share, a 58% increase over 2019.

- Closed on over $620 million in new acquisitions and additional investments at existing properties (including commitments to fund future development/redevelopment, but excluding transaction costs), including 20 new property acquisitions, expanding IIP’s footprint to 66 properties totaling 5.4 million rentable square feet in 17 states at year-end.

Fourth Quarter 2020 and Year-to-Date 2021 Highlights

Financial Results and Financing Activity

- Generated total revenues of approximately $37.1 million in the quarter, representing a 110% increase from the prior year’s quarter.

- Recorded net income attributable to common stockholders of approximately $21.0 million for the quarter, or $0.91 per diluted share, and AFFO of approximately $32.4 million, or $1.29 per diluted share (Note: beginning in the fourth quarter 2020, AFFO per diluted share includes the dilutive impact of the assumed full exchange of IIP’s $143.75 million of exchangeable senior notes for shares of common stock).

- Paid a quarterly dividend of $1.24 per common share on January 15, 2021 to stockholders of record as of December 31, 2020, representing a 24% increase from the prior year’s fourth quarter and a 6% increase from IIP’s third quarter 2020 dividend, and equal to an annualized dividend of $4.96 per share.

- Through IIP’s “at-the-market” equity offering program, issued 1,762,500 shares of common stock during the fourth quarter totaling approximately $262.9 million in net proceeds.

Investment and Leasing Activity

- From October 1, 2020 through today, made five acquisitions (including four new properties and additional land expansion at an existing property), totaling approximately 848,000 rentable square feet (including expected rentable square feet upon completion of properties under development/redevelopment), located in California, Florida, Massachusetts and Washington, and executed seven lease amendments to provide additional tenant improvements at properties located in Massachusetts, Michigan, New York, Ohio and Pennsylvania.

- In January 2021, executed a new long-term lease with Holistic Industries Inc. (Holistic) for IIP’s Los Angeles, California property, the prior tenant of which was under receivership, bringing IIP’s property portfolio to 100% leased.

- These five acquisitions, seven lease amendments and new lease at IIP’s Los Angeles property represented an aggregate additional investment by IIP of $254.1 million (consisting of purchase prices and commitments to fund future development and tenant improvements, but excluding transaction costs).

- In these transactions, established new tenant relationships with 4Front Ventures Corp. (4Front) and Harvest Health & Recreation Inc. (Harvest), while expanding existing tenant relationships with Green Peak Industries LLC, Green Thumb Industries Inc. (GTI), Holistic, Kings Garden Inc., LivWell Holdings, Inc. and PharmaCann Inc.

Balance Sheet Highlights (at December 31, 2020)

- Approximately $126.0 million in cash and cash equivalents and approximately $619.3 million in short-term investments, totaling approximately $745.3 million.

- No debt, other than approximately $143.75 million of 3.75% exchangeable senior notes maturing in 2024 (the Exchangeable Senior Notes), representing a fixed cash interest obligation of approximately $5.4 million annually, or approximately $1.3 million quarterly.

- 7.9% debt to total gross assets, with over $1.8 billion in total gross assets.

Rent Collections (as of February 24, 2021)

- IIP collected 100% of contractual rent due for the fourth quarter 2020 and 100% of contractual rent due for the months of January and February 2021 across IIP’s total portfolio, other than:

- The tenant at IIP’s Los Angeles, California property that was in receivership until IIP signed a new lease with Holistic for the entire property in January 2021; and

- Medical Investor Holdings, LLC (Vertical), the tenant at certain properties in southern California, which made partial payments of contractual rent due during these time periods. The properties that Vertical occupies represented less than one percent of IIP’s total gross assets at year-end.

- IIP has not provided deferrals of any rent obligations to any tenant since July 1, 2020.

Portfolio Update and Acquisition Activity

Portfolio Update

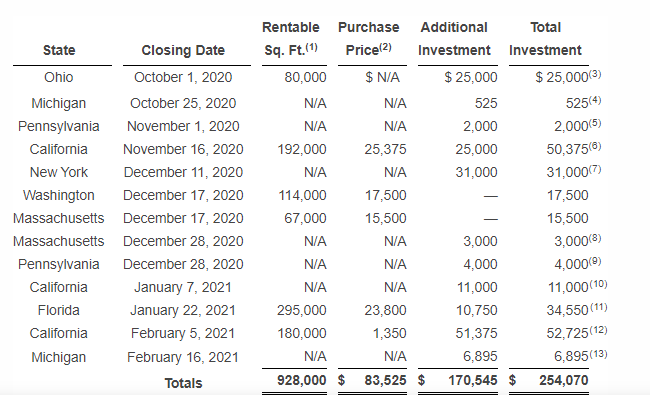

IIP acquired the following properties and made the following additional funds available to tenants for improvements at IIP’s properties during the period from October 1, 2020 through February 24, 2021 (dollars in thousands):

____________

(1) Includes expected rentable square feet at completion of construction for certain properties.

(2) Excludes transaction costs.

(3) The amount relates to a lease amendment which increased the tenant improvement allowance under a lease at one of IIP’s Ohio properties by $25.0 million to a total of $29.3 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. The additional tenant improvement allowance is expected to increase the property footprint by 80,000 square feet. As of February 24, 2021, IIP had funded approximately $7.6 million of the tenant improvement allowance.

(4) The amount relates to a lease amendment which increased the tenant improvement allowance under a lease at one of IIP’s Michigan properties by $525,000 to a total of approximately $1.8 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded approximately $1.7 million of the tenant improvement allowance.

(5) The amount relates to an amendment to IIP’s lease and development agreement which increased the construction funding at one of IIP’s Pennsylvania properties by $2.0 million to a total of approximately $27.1 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded all of the construction funding.

(6) The tenant is expected to complete tenant improvements at the property, for which IIP agreed to provide reimbursement of up to $25.0 million. As of February 24, 2021, IIP had not funded any of the reimbursement.

(7) The amount relates to an amendment to IIP’s lease and a development agreement which provides for construction funding at one of IIP’s New York properties of up to $31.0 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded approximately $70,000 of the construction funding.

(8) The amount relates to a lease amendment which increased the tenant improvement allowance under a lease at one of IIP’s Massachusetts properties by $3.0 million to a total of $5.0 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded $2.0 million of the tenant improvement allowance.

(9) The amount relates to a lease amendment which increased the tenant improvement allowance under a lease at one of IIP’s Pennsylvania properties by $4.0 million to a total of approximately $10.4 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded approximately $7.7 million of the tenant improvement allowance.

(10) The amount relates to a new lease executed at IIP’s Los Angeles, California property, which provides for a tenant improvement allowance of up to $11.0 million. As of February 24, 2021, IIP had not funded any of the tenant improvement allowance.

(11) The tenant is expected to complete tenant improvements at the property, for which IIP agreed to provide reimbursement of up to approximately $10.8 million. As of February 24, 2021, IIP had not funded any of the tenant improvement allowance.

(12) The amounts relate to the acquisition of additional land adjacent to an existing property and a lease amendment which provided a tenant improvement allowance and resulted in a corresponding adjustment to the base rent for the lease at the property. The tenant is expected to complete construction of two new buildings at the property comprising approximately 180,000 square feet in the aggregate, for which IIP agreed to provide reimbursement of up to approximately $51.4 million. As of February 24, 2021, IIP had not funded any of the tenant improvement allowance.

(13) The amount relates to a lease amendment which increased the tenant improvement allowance under a lease at one of IIP’s Michigan properties by approximately $6.9 million to a total of approximately $29.9 million, and also resulted in a corresponding adjustment to the base rent for the lease at the property. As of February 24, 2021, IIP had funded approximately $29.8 million of the tenant improvement allowance.

From January 1, 2020 through February 24, 2021, IIP made 22 acquisitions, located in California, Colorado, Florida, Illinois, Massachusetts, Michigan, New Jersey, Ohio, Pennsylvania, Virginia and Washington, and executed 23 lease amendments and a new lease to provide additional tenant improvements at IIP’s existing properties located in Arizona, California, Illinois, Maryland, Massachusetts, Michigan, Minnesota, New York, Ohio and Pennsylvania. These investments totaled approximately 2.8 million rentable square feet (including expected rentable square feet upon completion of properties under development/redevelopment).

As of February 24, 2021, IIP owned 67 properties located in Arizona, California, Colorado, Florida, Illinois, Maryland, Massachusetts, Michigan, Minnesota, Nevada, New Jersey, New York, North Dakota, Ohio, Pennsylvania, Virginia and Washington, totaling approximately 5.8 million rentable square feet (including approximately 2.0 million rentable square feet under development/redevelopment), which were 100% leased with a weighted-average remaining lease term of approximately 16.7 years. As of February 24, 2021, IIP had invested approximately $1.1 billion in the aggregate (excluding transaction costs) and had committed an additional approximately $328.7 million to reimburse certain tenants and sellers for completion of construction and tenant improvements at IIP’s properties.

Financing Activity

In November 2020, IIP entered into new equity distribution agreements with six sales agents, pursuant to which IIP may offer and sell from time to time through an “at-the-market” offering program up to $500 million in shares of its common stock. From November through today, IIP sold 1,762,500 shares of its common stock for net proceeds of approximately $262.9 million under this program.

IIP expects to use the net proceeds from the sales of these shares to invest in specialized industrial real estate assets that support the regulated medical-use cannabis cultivation and processing industry and for general corporate purposes.

Financial Results

IIP generated total revenues of approximately $37.1 million for the three months ended December 31, 2020, compared to approximately $17.7 million for the same period in 2019, an increase of 110%. IIP generated total revenues of approximately $116.9 million for the year ended December 31, 2020, compared to approximately $44.7 million for 2019, an increase of 162%. The increase in both periods was driven primarily by the acquisition and leasing of new properties, additional tenant improvement allowances and construction funding at existing properties resulting in adjustments to base rent, and contractual rental escalations at certain properties. Total revenues for the three months ended December 31, 2020 also included approximately $424,000 of the security deposit held by IIP at the properties leased to Vertical being applied to pay part of the rent and associated lease penalties owed by Vertical during this time period.

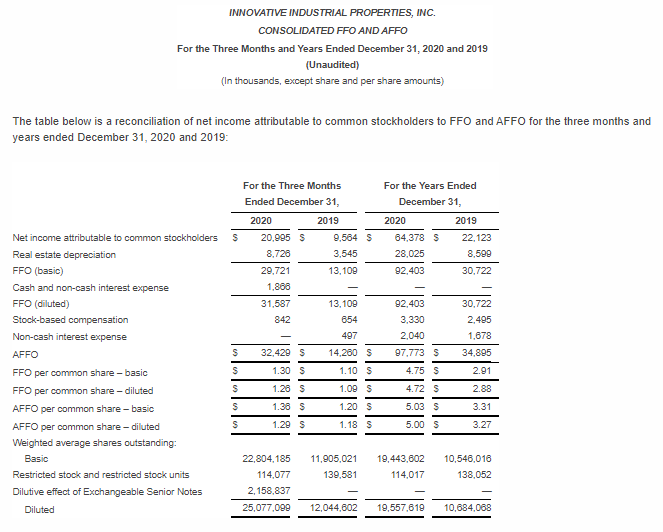

For the three months ended December 31, 2020, IIP recorded net income attributable to common stockholders and net income attributable to common stockholders per diluted share of approximately $21.0 million and $0.91, respectively; funds from operations (diluted) (“FFO”) and FFO per diluted share of approximately $31.6 million and $1.26, respectively; and AFFO and AFFO per diluted share of approximately $32.4 million and $1.29, respectively. Commencing in the fourth quarter 2020, FFO (diluted), AFFO and FFO and AFFO per diluted share include the dilutive impact of the assumed full exchange of the Exchangeable Senior Notes for shares of common stock, resulting in the “add-back” to FFO (diluted) from net income of approximately $1.9 million in cash and non-cash interest expense, and the addition of approximately 2.2 million shares to IIP’s total diluted share count for the quarter. The Exchangeable Senior Notes were anti-dilutive for purposes of calculating earnings per diluted share for all prior quarters, and as such, treated as anti-dilutive for purposes of calculating FFO, AFFO and FFO and AFFO per diluted share for all prior quarters.

For the year ended December 31, 2020, IIP recorded net income attributable to common stockholders and net income attributable to common stockholders per diluted share of $64.4 million and $3.27, respectively; FFO (diluted) and FFO per diluted share of $92.4 million and $4.72, respectively; and AFFO and AFFO per diluted share of approximately $97.8 million and $5.00, respectively. The Exchangeable Senior Notes were anti-dilutive for purposes of calculating earnings per diluted share for both 2020 and 2019, and as such, treated as anti-dilutive for purposes of calculating FFO, AFFO and FFO and AFFO per diluted share for both years.

FFO and AFFO are supplemental non-GAAP financial measures used in the real estate industry to measure and compare the operating performance of real estate companies. A complete reconciliation containing adjustments from GAAP net income attributable to common stockholders to FFO and AFFO and definitions of terms are included at the end of this release.

Teleconference and Webcast

Innovative Industrial Properties, Inc. will conduct a conference call and webcast at 10:00 a.m. Pacific Time (1:00 p.m. Eastern Time) on Thursday, February 25, 2021 to discuss IIP’s financial results and operations for the fourth quarter and year ended December 31, 2020. The call will be open to all interested investors through a live audio webcast at the Investor Relations section of IIP’s website at www.innovativeindustrialproperties.com, or live by calling 1-877-328-5514 (domestic) or 1-412-902-6764 (international) and asking to be joined to the Innovative Industrial Properties, Inc. conference call. The complete webcast will be archived for 90 days on IIP’s website. A telephone playback of the conference call will also be available from 12:00 p.m. Pacific Time on Thursday, February 25, 2020 until 12:00 p.m. Pacific Time on Thursday, March 4, 2021, by calling 1-877-344-7529 (domestic), 855-669-9658 (Canada) or 1-412-317-0088 (international) and using access code 10152350.

About Innovative Industrial Properties

Innovative Industrial Properties, Inc. is a self-advised Maryland corporation focused on the acquisition, ownership and management of specialized industrial properties leased to experienced, state-licensed operators for their regulated medical-use cannabis facilities. Innovative Industrial Properties, Inc. has elected to be taxed as a real estate investment trust, commencing with the year ended December 31, 2017. Additional information is available at www.innovativeindustrialproperties.com.

FFO and FFO per share are operating performance measures adopted by the National Association of Real Estate Investment Trusts, Inc. (NAREIT). NAREIT defines FFO as the most commonly accepted and reported measure of a REIT’s operating performance equal to net income, computed in accordance with accounting principles generally accepted in the United States (GAAP), excluding gains (or losses) from sales of property, depreciation, amortization and impairment related to real estate properties, and after adjustments for unconsolidated partnerships and joint ventures.

Management believes that net income, as defined by GAAP, is the most appropriate earnings measurement. However, management believes FFO and FFO per share to be important supplemental measures of a REIT’s performance because they provide an understanding of the operating performance of IIP’s properties without giving effect to certain significant non-cash items, primarily depreciation expense. Historical cost accounting for real estate assets in accordance with GAAP assumes that the value of real estate assets diminishes predictably over time. However, real estate values instead have historically risen or fallen with market conditions. IIP believes that by excluding the effect of depreciation, FFO and FFO per share can facilitate comparisons of operating performance between periods. FFO and FFO per share are used by management to evaluate the REIT’s operating performance and these measures are the predominant measures used by the REIT industry and industry analysts to evaluate REITs. For these reasons, management has deemed it appropriate to disclose and discuss FFO and FFO per share.

Management believes that AFFO and AFFO per share are also appropriate supplemental measures of a REIT’s operating performance. IIP calculates AFFO by adding to FFO certain non-cash and infrequent or unpredictable expenses which may impact comparability, consisting of non-cash stock-based compensation expense and non-cash interest expense generally.

For the three months ended December 31, 2020, FFO (diluted), AFFO and FFO and AFFO per diluted share include the dilutive impact of the assumed full exchange of the Exchangeable Senior Notes for shares of common stock. As a result, for purposes of calculating FFO (diluted), cash and non-cash interest expense of the Exchangeable Senior Notes totaling approximately $1.9 million was added back to FFO (diluted), and the total diluted weighted-average common shares outstanding increased by 2,158,837 shares for the period, which were the potentially issuable shares as if the Exchangeable Senior Notes were exchanged at the beginning of the period. These adjustments applied only for the three months ended December 31, 2020. The Exchangeable Senior Notes were anti-dilutive for purposes of calculating earnings per diluted share for all other periods presented, and as such, were treated as anti-dilutive for purposes of calculating FFO, AFFO and FFO and AFFO per diluted share for fiscal years 2020 and 2019 and the three months ended December 31, 2019.

IIP’s computation of FFO and AFFO may differ from the methodology for calculating FFO and AFFO utilized by other equity REITs and, accordingly, may not be comparable to such REITs. Further, FFO and AFFO do not represent cash flow available for management’s discretionary use. FFO and AFFO should not be considered as an alternative to net income (computed in accordance with GAAP) as an indicator of IIP’s financial performance or to cash flow from operating activities (computed in accordance with GAAP) as an indicator of IIP’s liquidity, nor is it indicative of funds available to fund IIP’s cash needs, including IIP’s ability to pay dividends or make distributions. FFO and AFFO should be considered only as supplements to net income computed in accordance with GAAP as measures of IIP’s operations.