As we described in a previous article, the Global Cannabis Stock Index melted down in December after a two-month rally. The index fell 29.0% and ended 2022 down a record decline of 70.4% for the year.

In this exclusive article we will summarize the performance of the other managed indices that New Cannabis Ventures offers to its readers. We will discuss the performance of the American Cannabis Operator Index, Ancillary Cannabis Index and Canadian Cannabis LP Index as well as Canadian Cannabis LP index Tier 1, 2 and 3.

American Cannabis Stocks Index

The American Cannabis Operator Index fell a stunning 40.8% in December to 14.25:

Down 22.9% in Q4, the index after the collapse in December, it was down 65.8% year-to-date, slightly ahead of the Global Cannabis Stock Index:

The index, which launched in October 2018, finally took out the low from March 2020:

During December, the strongest names all fell by less than 24% and included Charlotte’s Web (OTC: CWBHF) (TSX: CWEB), Schwazze (OTC: SHWZ) (CSE: SHWZ) and Upexi (NASDAQ: UPXI). Three stocks fell more than 55%: Jushi Holdings (OTC: JUSHF) (CSE: JUSH), Ayr Wellness (OTC: AYRWF) (CSE: AYR.A), and Columbia Care (OTC: CCHWF) (CSE: CCHW) (NOE: CCHW). There are no changes to the index, which has 16 members, for the month ahead.

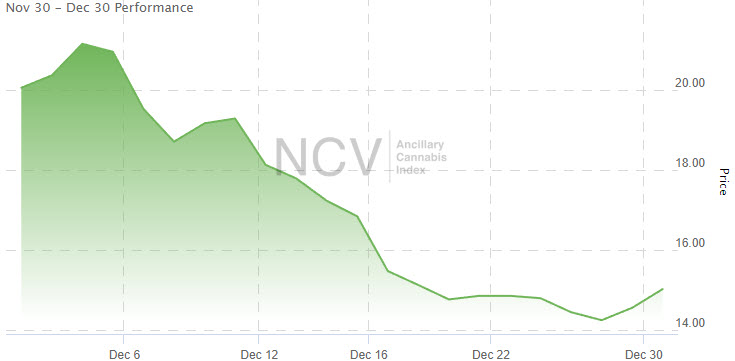

Ancillary Cannabis Index

The Ancillary Cannabis Index was the worst part of the market during 2022, but it fared better than other sub-sectors in December, dropping 25.1% to 15.02:

The index was down 76.6% in 2022:

The index is down almost 85% since launching at the end of March in 2021:

During December, the best performing stocks, all down by 7.6% or less, were Turning Point Brands (NYSE: TPB), Chicago Atlantic Real Estate Finance (NASDAQ: REFI) and Leafly (NASDAQ: LFLY). The largest decliners, all falling by more than 42%, were Agrify (NASDAQ: AGFY), SHF Holdings (NASDAQ: SHFS) and GrowGeneration (NASDAQ: GRWG). In January, Agrify, Leafly and SHF Holdings will leave the index, which will have now 8 members.

Canadian Cannabis LP Index

The Canadian Cannabis LP Index gave up a lot less ground than the American Cannabis Operator Index, falling 19.2% to 72.59:

The index lost 11.4% during Q4, and it declined 62.8% in 2022 from its year-end 2021 close of 194.95:

It broke to a new all-time low during the month, and it is down a lot from the peak:

Canadian Cannabis LP Tier 1 Index

During November, Tier 1, which includes 5 large revenue generators, dropped 8.1%, and this index collapsed 33.6% in December to 88.14. Tier 1, which was down 72.0% in 2022, dropped 17.7% in 2021 when it ended at 314.28. Among Tier 1 companies, Cronos Group (TSX: CRON) (NASDAQ: CRON), down 17.3%, was the best performer, while HEXO Corp. (TSX: HEXO) (NASDAQ: HEXO) was the worst performer again, falling 54.9%.

Canadian Cannabis LP Tier 2 Index

Tier 2 index advanced by 0.3% in November, and it dropped by 14.8% in December to 109.79. In 2021, it lost 17.1%, closing at 267.36, and it fell 58.9% in 2022. Among Tier 2 companies, the worst stock was Entourage Health (TSXV: ENTG) (OTC: ETGRF) again, which fell 42.9%, while the best performing stock was Rubicon Organics (TSXV: ROMJ) (OTC: ROMJF), which gained 18.5%.

Canadian Cannabis LP Tier 3 Index

Tier 3 index dropped 14.1% in November, and it fell 16.2% in December to 17.66. It ended at 47.42 in 2021, declining 19.9%, and was now down 62.8% in 2022. Among Tier 3 companies, Canadabis Capital (TSXV: CANB) gained 128.6%, while two stocks lost more than 48% of their value: The Green Organic Dutchman (CSE: TGOD) (OTC: TGODF) and IM Cannabis (CSE: IMCC) (NASDAQ: IMCC).

New Cannabis Ventures maintains seven proprietary indices designed to help investors monitor the publicly-traded cannabis stocks, including the Global Cannabis Stock Index as well as the Canadian Cannabis LP Index and its three sub-indices. The sixth index, the American Cannabis Operator Index, was launched at the end of October 2018 and tracks the leading cultivators, processors and retailers of cannabis in the United States. Afterwards, we introduced the Ancillary Cannabis Index at the end of March 2021, reflecting the increasing number of publicly-traded companies providing goods or services to cannabis operators.