![]() Visit the OrganiGram Investor Dashboard and stay up to date with data-driven, fact based due diligence for active traders and investors.

Visit the OrganiGram Investor Dashboard and stay up to date with data-driven, fact based due diligence for active traders and investors.

Organigram Reports Second Quarter Fiscal 2020 Results

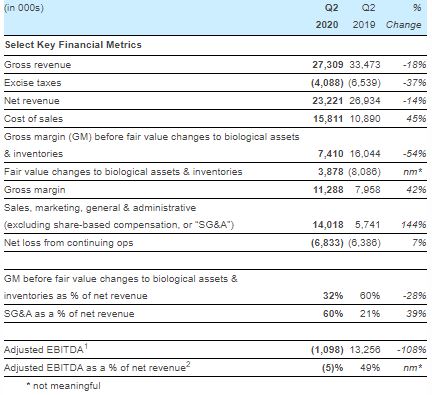

- Net revenue of $23.2 million compared to $26.9 million in Q2 2019 and $25.2 million in Q1 2020

- Adult-use recreational net revenue sequentially grew 16% to $15.0 million from $12.9 million in Q1 2020

- Ended quarter with $41.2 million in cash and short-term investments

- First shipped its Rec 2.0 products with Trailblazer Torch vape cartridges in December 2019, followed by Edison Feather ready-to-go distillate vape pens and Edison Bytes, cannabis-infused chocolates, in February 2020

- Expect Edison PAX ERA distillate cartridges to start shipping in Q2 calendar 2020

- Subsequent to quarter-end, received licensing for the remainder of Phase 5, which includes a dedicated edibles and derivatives facility

- Announced a corporate action plan intended to boost containment of the COVID-19 virus and protect the health of employees as well as maintain sufficient business continuity to meet anticipated demand for its products during this period

MONCTON, New Brunswick, April 14, 2020–(BUSINESS WIRE)–Organigram Holdings Inc. (NASDAQ: OGI) (TSX: OGI), the parent company of Organigram Inc. (together, the “Company” or “Organigram”), a leading licensed producer of cannabis, is pleased to announce its results for the second quarter ended February 29, 2020 (“Q2” or “Q2 2020”).

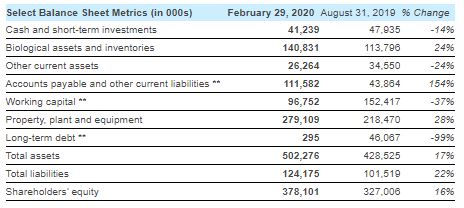

** In accordance with IFRS, the Company has classified the long-term portion of the BMO term loan ($76.4 million) to current liabilities as the Company was in violation of one of the financial covenants contained in the agreement governing the term loan. The Company obtained a waiver from its lenders that waives compliance with this covenant until May 30, 2020. See “Liquidity and Capital Resources” section in this press release.

Our second quarter results reflect continued execution despite ongoing industry challenges. We introduced new products such as our Edison Bytes chocolates, Edison Limelight dried flower and Trailblazer vape pens and continue to elevate the Canadian consumer’s cannabis experience. These products have been well received with strong customer demand to date and we look forward to further roll-outs in the space.

Greg Engel, CEO

Greg Engel, CEO

The Company continues to diversify its revenue streams. During the quarter traditional Rec 1.0 products in the adult-use recreational space represented 52% of net revenue (91% in Q2 2019). New Rec 2.0 products (chocolates, vape pens) in the adult-use recreational space represented 13% of net revenue (0% in Q2 2019). Wholesale sales to other large Canadian Licensed Producers represented 24% (0% in Q2 2019) with Canadian medical sales representing 10% (9% in Q1 2019) and international sales representing 1% (0% in Q2 2019). The Company continues to pursue additional opportunities to expand its product mix and customer base.

Key Financial Results for the Second Quarter Fiscal 2020

Net Revenue:

- Q2 2020 net revenue of $23.2 million compared to $26.9 million in Q2 2019 primarily due to: lower recreational flower and oil sales volumes compared to Q2 2019 when the timing of large pipeline fill orders to Alberta and Ontario occurred to fulfill supply shortages following the legalization of adult-use recreational cannabis sales; lower average net selling price from increased competition; and evolving consumer preferences, for which a provision for returns and price adjustments was recorded in Q2 2020, mostly related to cannabis oil. This was partially offset by the launch of Rec 2.0 products (vape products and cannabis-infused chocolates), and higher medical revenues as well as wholesale and international revenues, which had not occurred in the prior comparative quarter.

Cost of Sales:

- Q2 2020 cost of sales of $15.8 million compared to Q2 2019 cost of sales of $10.9 million.

- Higher cost of sales in Q2 2020 was primarily due to: higher post-harvest costs, initial production inefficiencies resulting from the launch of vapes and chocolates (which may persist in the near term), and inventory provisions and write-offs of approximately $1.3 million.

Gross Margin before fair value changes to biological assets and inventories sold:

Q2 2020 gross margin before fair value changes to biological assets and inventories of $7.4 million, or 32% of net revenue, compared to $16.0 million in Q2 2019, or 60% of net revenue.

Lower gross margin and lower gross margin as a percentage of net revenue in Q2 2020 were largely due to lower net revenue and higher cost of sales as described above.

Gross Margin:

- Q2 2020 gross margin of $11.3 million compared to Q2 2019 gross margin of $8.0 million, largely due to a net non-cash fair value gain on biological assets and inventories sold of $3.9 million in Q2 2020 versus a net non-cash fair value loss of $8.1 million in Q2 2019.

Sales, Marketing, General and Administrative Expenses (“SG&A”):

- Q2 2020 SG&A of $14.0 million compared to $5.7 million in Q2 2019 as the Company invested more in the marketing and promotion of its product portfolio while also scaling its operations for the launch of its Rec 2.0 line of products.

- Q2 2020 SG&A represented 60% of net revenue compared to 21% in Q2 2019 primarily due to higher SG&A expenses in Q2 2020 and higher net revenue in Q2 2019 (both as described above).

Adjusted EBITDA²:

- Q2 2020 negative adjusted EBITDA of $1.1 million compared to Q2 2019 adjusted EBITDA of $13.3 million.

- Q2 2020 negative adjusted EBITDA was largely impacted by higher cost of sales and SG&A expenses in Q2 2020 as described above.

Net Loss from Continuing Operations:

- Q2 2020 net loss of $6.8 million, or $(0.041) per share on a diluted basis, compared to Q2 2019 net loss of $6.4 million, or $(0.049) per share, largely due to higher SG&A expenses in Q2 2020 as described above.

Key Commentary on Q2 2020 Results vs Q1 2020

- Q2 2020 net revenue of $23.2 million compared to Q1 2020 net revenue of $25.2 million, with adult-use recreational sales up approximately $2.1 million or 16% offset by a decrease in wholesale revenue. Q2 2020 net revenue of $23.2 million was largely comprised of $15.0 million in sales to the adult-use recreational market, $2.4 million in sales to the medical market, $5.6 million in wholesale revenue, and $0.2 million in international sales. This compared to Q1 2020 net revenue of $25.2 million, largely comprised of $12.9 million in sales to the adult-use recreational market, $2.7 million in sales to the medical market, $9.2 million in wholesale revenue, and $0.3 million in international sales.

- Q2 2020 cash and “all-in” costs of cultivation of $0.53 and $0.75 per gram of dried flower harvested³, respectively, decreased from $0.61 and $0.87 per gram in Q1 2020, respectively, as more economies of scale were realized with expanded cultivation capacity and as the yield per plant⁴ increased from 150 grams in Q1 2020 to 155 grams in Q2 2020.

- Q2 2020 cost of sales remained flat at $15.8 million from Q1 2020 (despite lower net revenue in Q2 2020 compared to Q1 2020) due to higher post-harvest costs due to: a lower percentage of less costly wholesale product sold (as wholesale is packaged in bulk without any specific labeling and excise stamps); and the launch of Rec 2.0 products in Q2 2020, as the Company scales and optimizes production and packaging.

- Q2 2020 gross margin before fair value changes to biological assets and inventory decreased to $7.4 million, or 32% of net revenue, from Q1 2020 gross margin before fair value changes of $9.3 million, or 37%, largely due to inventory provisions and write-offs of approximately $1.3 million.

- Q2 2020 gross margin of $11.3 million remained stable with Q1 2020 gross margin, largely due to lower non-cash fair value changes in biological assets and inventories in Q1 2020, which offset higher net revenue and a stable cost of sales figure from quarter to quarter.

- Q2 2020 SG&A of $14 million, or 60% of net revenue, compared to Q1 2020 SG&A of $9.4 million, or 37% of net revenue, as Q2 2020 included higher costs related to a large brand marketing campaign and costs related to the launch of Rec 2.0 products.

- Q2 2020 negative adjusted EBITDA⁵ of $1.1 million compared to Q1 2020 adjusted EBITDA of $4.9 million. Q2 2020 negative adjusted EBITDA was impacted by a lower gross margin before fair value changes to biological assets and inventories (described above) and higher SG&A compared to Q1 2020 (described above).

Adult-Use Recreational Launch 2.0 (“Rec 2.0”) – Derivative and Edible Products

- Organigram shipped the first of its Rec 2.0 products on or about December 17, 2019 including Trailblazer Spark, Flicker and Glow 510-thread Torch vape cartridges followed by its first shipment of Edison + Feather ready-to-go distillate pens on or about February 20, 2020. Powered by Feather technology, Edison vape pens are ready-to-use inhalation-activated pens that are designed to offer adult consumers a simple and intuitive user experience.

- The Company continues to expect to launch Edison + PAX ERA® distillate cartridges, its premium line of vape products, in Q2 calendar 2020.

- The Company also began shipping the first of its premium cannabis-infused chocolates, Edison Bytes, which are truffles in both milk and dark chocolate formulations on or about February 20, 2020. The chocolates are available to Canadian adult consumers as single chocolates containing 10 mg of THC each and as a set of two truffles containing 5 mg THC each.

- As previously announced, Organigram’s researchers have developed a proprietary nano-emulsification technology that is anticipated to provide an initial absorption of the cannabinoids within 10 to 15 minutes. The team of researchers transformed this emulsification into a solid form, turning it into a dissolvable powder which can be added to a liquid of a consumer’s choice. The Company is no longer able to provide guidance on specific launch timing for its powdered beverage product (previously expected to launch in Q2 calendar 2020) due to the uncertainty of the impact and duration of the COVID-19 situation.

Phase 4 Expansion

- The complete Phase 4 expansion of the Moncton Campus facility represents a total of 77,000 kg per year of additional annual target production capacity⁶ and has been divided into a series of stages (4A: 25,000 kg; 4B: 28,000 kg; and 4C: 24,000 kg).

- Construction of Phases 4A and 4B has been completed and licensing approval from Health Canada received for total target licensed cultivation capacity of 89,000 kg per year⁶ (once fully operational) as of the date of this press release. The Company’s management has decided to fill these new rooms at a slower pace in response to lower than anticipated consumer demand at this time (which the Company believes is largely due to the lack of an adequate retail store network) and due to a reduced workforce at the Moncton Campus facility (to boost COVID-19 containment efforts). The Company will continue to closely monitor market conditions and the evolving pandemic.

- As first disclosed with the release of Organigram’s Q4 Fiscal 2019 results on November 25, 2019, the Company’s management made a strategic decision to delay final completion of Phase 4C (the final stage of the Phase 4 expansion), previously targeted for the end of calendar 2019, largely due to lower than anticipated consumer demand noted above and to more effectively manage and prioritize cash flow as well as potentially use the space in Phase 4C for other opportunities (if strategic and/or market factors dictate).

- The estimated capital cost to complete Phase 4, such that 4C can be occupied and used for other potential purposes, was approximately $2 million as of quarter-end.

Phase 5 Under Refurbishment

- Phase 5, once fully operational, is expected to add significant functionality to the Moncton Campus including additional post-harvesting rooms (including drying rooms), additional extraction capacity, and a dedicated derivatives and edibles facility.

- During the quarter, the Company received Health Canada’s approval for the licensing of the expanded site perimeter, including Phase 5, as well as approval for the operations area that houses the Company’s chocolate production line. Additional drying and storage areas were also added to the License.

- Subsequent to quarter-end, the Company received Health Canada’s licensing approval for the remainder of Phase 5. The license amendment includes the approval of a two-floor production facility designed to support all processing activity as well as dedicated spaces for packaging of flower, pre-rolls, vape pens and powdered beverages. The amendment to the License also allows for new purpose-built harvest and drying rooms and support areas for quality assurance, maintenance and sanitation.

- The estimated capital cost to complete Phase 5 was approximately $11 million as at quarter-end, largely related to the installation of certain equipment in the edibles and extraction area. Although the Company intends to complete the build-out of Phase 5, funds will be expended at a slower pace to balance near-term priorities with respect to COVID-19.

COVID-19 Corporate Action Plan

- On April 7, 2020, Organigram announced the temporary layoff of approximately 45 per cent of its workforce or approximately 400 employees primarily to help boost COVID-19 containment efforts. The Company has offered voluntary layoffs to certain staff and those that accepted made up the majority of the layoffs. In some cases, due to the impacts of COVID-19, some administrative, support and other functions were deemed non-essential to the short-term needs of the business. The temporary layoffs were initiated on March 24, 2020 and the Company will continuously monitor the evolving situation.

- Lump-sum payments (equating to approximately two weeks worth of work) have been paid to the affected employees to help bridge the gap to available government programs. In addition, the Company will absorb the employee paid portion of health, dental and short-term disability premiums for all employees during this difficult time. The impact of these temporary layoffs will result in a one-time charge of approximately $0.6 million during the month of April 2020, which is primarily associated with the lump sum payments provided to these employees⁷.

- The Company plans to maintain an experienced group of employees at its Moncton facility with skills flexible enough to work on various production and packaging lines to help fulfill the anticipated provincial demand levels.

- Organigram, which operates one facility in Moncton, New Brunswick as well as offices in Moncton, Toronto and Ottawa, has already taken actions as recommended by Public Health Agency of Canada and the provincial Public Health authorities which include, but are not limited to: the establishment of an Emergency Response Team; the implementation of a work from home policy, physical distancing protocols; restrictions on large gatherings and travel; increased sanitation; and mandatory reporting of any employee absences, including any COVID-19 symptoms.

Outlook

- During the temporary lay-off of employees due to COVID-19, Organigram expects reductions to cultivation, harvest, production and packaging capacity but plans to supplement with inventories on hand to meet anticipated demand. Specifically, the Company will be focused on leveraging the automated and the most efficient lines of production and will deprioritize products with lower margins and/or that require higher manual labour.

- The Company believes it has sufficient inventory levels to supplement reduced harvest plans and enough contingency staff to keep packaging capacity intact in order to meet anticipated demand in the short-term. The Company also remains comfortable with its current inventory levels from external suppliers (e.g. vape product hardware, packaging materials) and has not experienced any significant disruptions to date.

Liquidity and Capital Resources

- Organigram had $41.2 million in cash and short-term investments at quarter-end. The Company believes its current capital sources, expected future capital sources and its ability to manage cash flow and working capital levels will allow it to meet its current and future obligations, to meet expected debt service requirements, and to fund its operating and capital expenditure plans.

- Working capital as at quarter-end, of $96.8 million compared to $152.4 million as at August 31, 2019, was largely due to an IFRS requirement to classify the long-term portion of the BMO term loan ($76.4 million) to current liabilities as the Company was in non-compliance with one of its financial covenants. The Company obtained a covenant waiver from its lenders that waives compliance with the financial covenant in question until May 30, 2020 and is currently negotiating an amendment to its credit facility agreement in an effort to address this matter. While the Company believes it will be successful in negotiating the amendment, there can be no guarantee that an amendment will be secured on terms favourable to the Company or at all.

- The Company reported approximately $85.2 million in current and long-term debt as at quarter-end, which primarily represents the carrying value of its term loan in its credit facility with BMO and a syndicate of lenders. As of the date of this press release, $30.0 million remains undrawn on the term loan in its credit facility.

- The credit facility also includes a $25 million revolver for general corporate and working capital purposes. Availability under the revolver is based on a percentage of the trade receivables at the end of each month and is undrawn as of the date of this press release.

- On December 4, 2019, Organigram announced it had established an ATM program pursuant to a prospectus supplement to its base shelf prospectus. The supplement allowed the Company to issue up to $55 million (or its U.S. dollar equivalent) of common shares from treasury from time to time, at the Company’s discretion. The Company issued approximately 16.2 million Common Shares pursuant to the ATM Program during the three months ended February 29, 2020 for gross proceeds of approximately $55.0 million at a weighted average price of $3.39 per Common Share. Net proceeds realized were $52.9 million after agents’ commissions, regulatory and legal and professional fees. Proceeds were raised in both USD (for shares sold through the NASDAQ) and CAD (for shares sold through the TSX) and the weighted average share price was calculated using the spot rate on the day of settlement. The Company has used, and intends to continue to use, the net proceeds to fund capital projects, for general corporate purposes and to repay indebtedness. The ATM Program was completed prior to quarter-end.

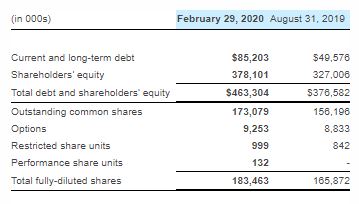

Capital Structure

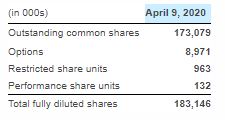

Outstanding basic and fully diluted share count as at April 9, 2020 is as follows:

Second Quarter Fiscal 2020 Conference Call

The Company will host a conference call to discuss its results with details as follows:

Date: April 14, 2020

Time: 8:00 a.m. Eastern Standard Time

Toll Free (North America) Dial-In Number: 1-866-211-4093

International Dial-In Number: 647-689-6727

Webcast: https://event.on24.com/wcc/r/2158457/26EA11F1C003A07ED88A32124DC3CB15

A replay of the webcast will be available within 24 hours after the conclusion of the call at https://www.organigram.ca/investors and will be archived for a period of 90 days following the call.

Non-IFRS Financial Measures

This news release refers to certain financial performance measures (including yield per plant (in grams), target production capacity, adjusted EBITDA and cash and “all-in” cost of cultivation) that are not defined by and do not have a standardized meaning under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. These non-IFRS financial performance measures are defined below. Non-IFRS financial measures are used by management to assess the financial and operational performance of the Company. The Company believes that these non-IFRS financial measures, in addition to conventional measures prepared in accordance with IFRS, enable investors to evaluate the Company’s operating results, underlying performance and prospects in a similar manner to the Company’s management. As there are no standardized methods of calculating these non-IFRS measures, the Company’s approaches may differ from those used by others, and accordingly, the use of these measures may not be directly comparable. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Please refer to the Company’s Q2 2020 MD&A for definitions and, in the case of adjusted EBITDA, a reconciliation to IFRS amounts.

About Organigram Holdings Inc.

Organigram Holdings Inc. is a NASDAQ Global Select Market and a Toronto Stock Exchange (“TSX”) listed company whose wholly owned subsidiary, Organigram Inc., is a licensed producer of cannabis and cannabis-derived products in Canada.

Organigram is focused on producing high-quality, indoor-grown cannabis for patients and adult recreational consumers in Canada, as well as developing international business partnerships to extend the Company’s global footprint. Organigram has also developed a portfolio of adult use recreational cannabis brands including The Edison Cannabis Company, Ankr Organics and Trailblazer. Organigram’s primary facility is located in Moncton, New Brunswick and the Company is regulated by Health Canada under the Cannabis Act (Canada) and the Cannabis Regulations (Canada).

¹Adjusted EBITDA and adjusted EBITDA as a percentage of net revenue (adjusted EBITDA margin %) are non-IFRS financial measures not defined by and do not have any standardized meaning under IFRS; please refer to the Company’s Q2 2020 MD&A for definitions and a reconciliation to IFRS.

²Adjusted EBITDA is a non-IFRS financial measure not defined by and does not have any standardized meaning under IFRS; please refer to the Company’s Q2 2020 MD&A for definitions and a reconciliation to IFRS.

³Cash and “all-in” costs of cultivation per gram of dried flower harvested are non-IFRS measures that are not defined by and do not have any standardized meaning under IFRS. “Cost of cultivation” per gram harvested includes “cash” costs such as direct labour, direct materials and manufacturing overhead (e.g. maintenance) as well as “non-cash” expenses such as employee share-based compensation for cultivation employees and depreciation related to buildings and equipment of the production facility. Cost of cultivation does not include packaging costs, which are added to arrive at the cost for inventory, nor distribution costs (shipping), both of which are included in the cost of sales. Thus, readers are cautioned against comparing cost of cultivation per gram harvested with cost of sales for the same period(s) for at least two reasons: (1) Cost of sales includes packaging costs and distribution (shipping) costs which “Cost of cultivation” does not, and (2) there is a delay between when product is harvested and when it is sold which can be one or two quarters (or longer with extraction material). Cost of cultivation also does not include indirect production costs, which are expensed directly against gross margin.

⁴Yield per plant (in grams) is a non-IFRS operational performance measure not defined by and does not have any standardized meaning under IFRS; please refer to the Company’s Q2 2020 MD&A for definition.

⁵Adjusted EBITDA is a non-IFRS financial measure not defined by and does not have any standardized meaning under IFRS; please refer to the Company’s Q2 2020 MD&A for definitions and a reconciliation to IFRS amounts.

⁶Target production capacity is a non-IFRS operational performance measure not defined by and does not have any standardized meaning under IFRS; please refer to the Company’s Q2 2020 MD&A for definition.

⁷These numbers are subject to change as additional employees elect to take a temporary layoff in response to COVID-19. In the event that these employees are not recalled, and the employment relationship is deemed terminated the Company would remain liable for termination and/or severance payments.

For fact-based information on Organigram, view the company’s sponsored Investor Dashboard.