You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to...

The cannabis industry faces several significant burdens, though perhaps none as onerous as 280E, an antiquated tax rule that prohibits companies that grow, process or sell cannabi from deducting...

Bipartisan Members of U.S. Senate and House Introduce Sweeping Measures to Reform Marijuana Policy and Support Cannabis Businesses In a key development, Rep. Carlos Curbelo (R-FL), Republican member of...

Taxation of the Regulated Cannabis Industry: Searching for a Higher Authority Guest post by Daniel F. Rahill, Managing Director, Midwest Tax Practice Leader of Alvarez & Marsal Taxand, LLC...

Analysis of COGS for Canna-Business Owners Guest post by Derek Davis, CPA Cost of Goods Sold (COGS) deductions can offer some substantial tax savings for your business, as the...

Blum Oakland Pays an Astonishing Effective Tax-Rate of 966% Entrepreneurs and investors in the cannabis industry face a litany of obstacles, but one of the worst is an antiquated tax...

Fighting the Feds, Round Two: Harborside vs. the IRS Industry threatened as nation’s model dispensary attacked over obscure tax code, 280E OAKLAND, Calif., Jun 04, 2016 (GLOBE NEWSWIRE via...

This article marks the end of this series’ emphasis on income tax. After introducing section 280E’s confiscatory effect, identifying the need for cannabis enterprise to maximize cost of goods...

I finished Part 2 of this series emphasizing section 280E’s principle force. Section 280E does not universally bar illegal commercial enterprises from deducting necessary and ordinary business expenses. Rather,...

Last week I introduced the conflict between federal income tax law and state-sanctioned cannabis enterprises here and here. In brief, the Internal Revenue Code (“Code”) section 280E proscribes state-sanctioned...

Mike Parnes, Attorney at Barth Daly LLP With the recent legalization of recreational cannabis sales in Alaska, Colorado, Oregon, and Washington, the writing is on the wall for the...

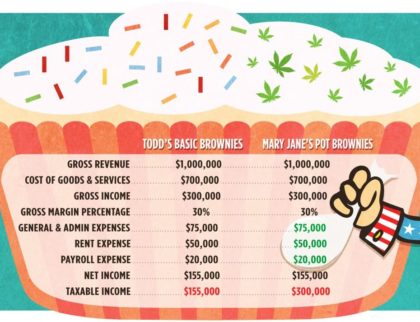

This comparison shows how a marijuana bakery can’t claim federal deductions a typical bakery can claim. Items in green cannot be deducted. (Image courtesy of wweek.com) The long lines and eager...