![]()

TerrAscend Reports Record Fourth Quarter and Full Year 2022 Net Revenue

- Fourth quarter 2022 record Net Revenue of $69.0 million, an increase of 50.3% year-over-year and 4.2% quarter-over-quarter

- Fourth quarter 2022 positive cash flow from operations of $7.3 million compared to $1.5 million in the third quarter of 2022

- Reduced debt by $80 million during the quarter

- Submitted application to up-list to the Toronto Stock Exchange (TSX)

TORONTO, March 16, 2023 /CNW/ – TerrAscend Corp. (“TerrAscend” or the “Company”) (CSE: TER) (OTCQX: TRSSF), a leading North American cannabis operator, today reported its financial results for the fourth quarter and full year ended December 31, 2022. All amounts are expressed in U.S. dollars and are prepared under U.S. Generally Accepted Accounting Principles (GAAP), unless indicated otherwise.

The following financial measures are reported as results from continuing operations due to the shutdown of the licensed producer business in Canada, which is reported as discontinued operations for all of 2022. All historical periods have been restated accordingly.

Fourth Quarter 2022 Financial Highlights

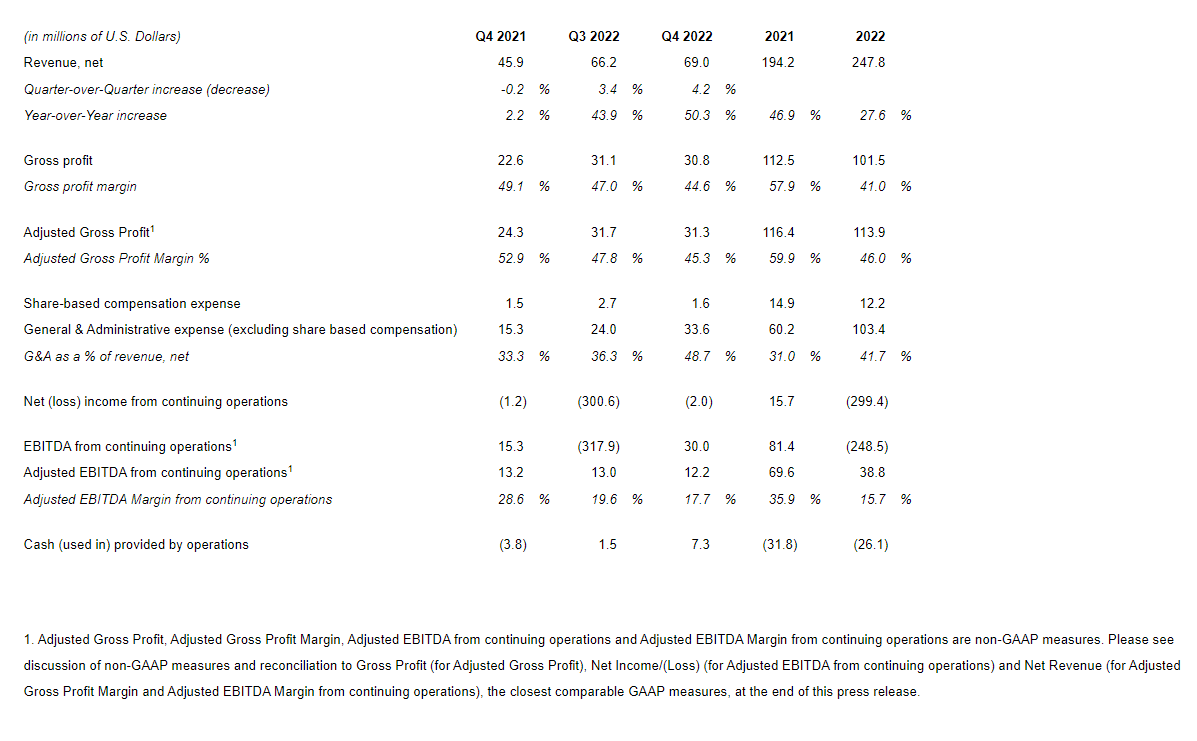

- Net Revenue was $69.0 million, an increase of 4.2% sequentially and 50.3% year-over-year.

- Gross Profit Margin was 44.6%, compared to 47.0% in Q3 2022 and 49.1% in Q4 2021.

- Adjusted Gross Profit Margin1 was 45.3%, compared to 47.8% in Q3 2022 and 52.9% in Q4 2021.

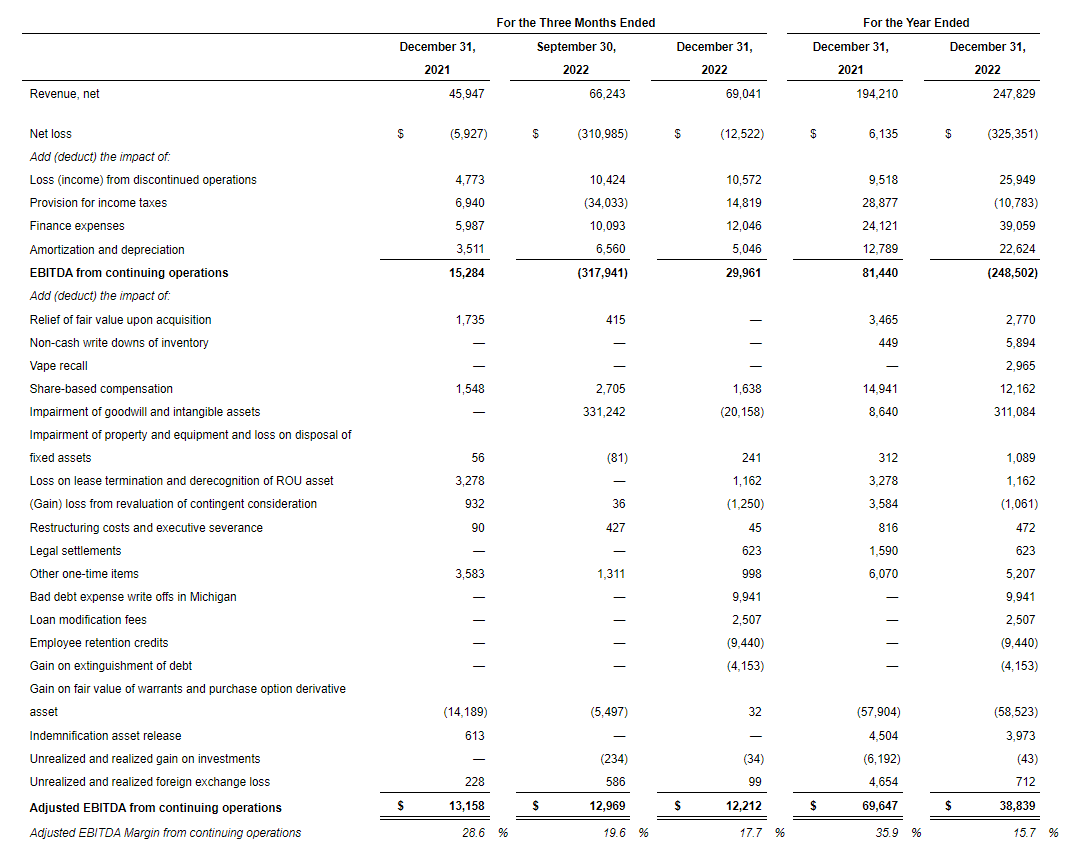

- GAAP Net loss from continuing operations was $2.0 million, compared to a net loss of $300.6 million in Q3 2022 and a net loss of $1.2 million in Q4 2021. As previously reported, a $331.2 non-cash impairment charge was recorded in Q3 2022 against goodwill and intangibles for the Company’s Michigan business, which was reduced by $20.2 million in Q4 2022 as a result of the finalization of the fair value of net assets acquired.

- EBITDA from continuing operations1 was $30.0 million, compared to ($317.9) million in Q3 2022 and $15.3 million in Q4 2021. As previously reported, a $331.2 non-cash impairment charge was recorded in Q3 2022 against goodwill and intangibles for the Company’s Michigan business, which was reduced by $20.2 million in Q4 2022 as a result of the finalization of the fair value of net assets acquired.

- Adjusted EBITDA from continuing operations1 was $12.2 million, compared to $13.0 million in Q3 2022 and $13.2 million in Q4 2021.

- Adjusted EBITDA Margin from continuing operations1 was 17.7%, compared to 19.6% in Q3 2022 and 28.6% in Q4 2021.

- Cashflow from Operations was a positive $7.3 million compared to a positive $1.5 million in Q3 2022 and negative $3.8 million in Q4 2021.

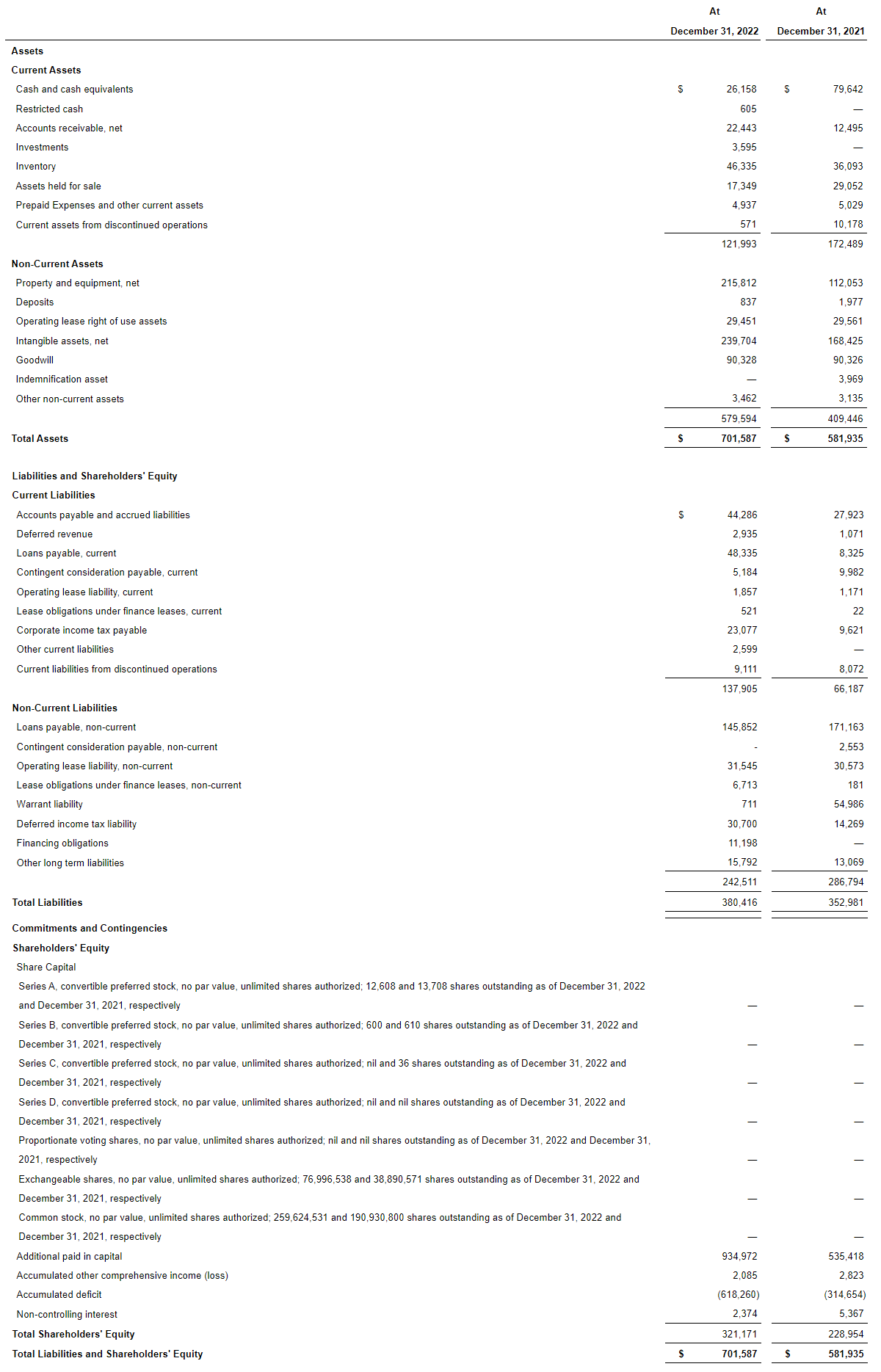

- Cash and Cash Equivalents, totaled $26.2 million as of December 31, 2022.

- Principal amounts of loans payable were $205.3 million as of December 31, 2022 compared to $284.2 million as of September 30, 2022.

Full Year 2022 Financial Highlights

- Net Revenue was $247.8 million, an increase of 27.6% year-over-year.

- Gross Profit Margin was 41.0% compared to 57.9% in 2021.

- Adjusted Gross Profit Margin1 was 46.0% compared to 59.9% in 2021.

- GAAP Net Loss from continuing operations was $299.4 million compared to net income of $15.7 million in 2021. In 2022, a $311.1 non-cash impairment charge was recorded against goodwill and intangibles for the Company’s Michigan business.

- EBITDA from continuing operations1 was ($248.5) million, compared to $81.4 million in 2021. In 2022, a $311.1 non-cash impairment charge was recorded against goodwill and intangibles for the Company’s Michigan business.

- Adjusted EBITDA from continuing operations1 was $38.8 million compared to $69.6 million in 2021.

- Adjusted EBITDA Margin from continuing operations1 was 15.7% compared to 35.9% in 2021.

- Cashflow from Operations was a negative $26.1 million compared to a negative $31.8 million in 2021.

I am pleased that despite a challenging environment throughout most of 2022, we delivered record annual revenue of $248 million, an increase of 28% year-over-year. Revenue grew sequentially every quarter throughout the year, culminating in a record fourth quarter of $69 million, an increase of 50% year-over-year.

Jason Wild, Executive Chairman of TerrAscend

Jason Wild, Executive Chairman of TerrAscend

Perhaps most noteworthy was that, in addition to an $80 million reduction in debt during the quarter, Q4 2022 also marked our second consecutive quarter of generating positive cashflow from operations. Looking ahead, we expect the distress in the industry to lead to opportunities for us to pivot our deep not wide strategy to a deep and wide strategy, on our terms.

Financial Summary Q4 2022, Full Year 2022 and Comparative Periods

All figures are restated for the Canadian business recorded as discontinued operations.

Fourth Quarter 2022 Business and Operational Highlights

- Closed on a non-brokered senior secured term loan in an aggregate principal amount of $45.5 million with Pelorus Equity Group.

- Paid down $30 million of debt related to Michigan term loan with Chicago Atlantic.

- Converted $90 million of debt with Canopy Growth to exchangable shares at CAD$5.10 per share.

- Amended certain terms of Ilera term loan, which afforded the Company the flexibilty to enter into a sale leaseback or mortgage on it’s Pennsylvania cultivation facility in return for a $5 million pay down in Q4 2022, and a commitment for an early pay down of $35 million in Q1 2023, with no pre-payment fees, which was further amended subsequent to the quarter.

- Listed 67,000 square foot Mississuaga, Ontario facility for sale at a price of CAD$24.3 million.

- Opened fourth Michigan Cookies Dispensary in Jackson.

- Appointed Ira Duarte to the Board of Directors. Ms. Duarte will also serve as Chair of the Audit Committee.

Subsequent Events

- Applied to list common shares on the Toronto Stock Exchange (TSX), upon completion of a reorganization which is expected to qualify the Company for listing, subject to shareholder approval at the Company’s annual general meeting to be scheduled in June, and subject to TSX approval.

- Signed non-binding term sheet with a commercial bank for a $25 million mortgage on Pennsylvania cultivation facility at a 9.25% fixed rate.

- Amended certain terms of Ilera term loan to extend the early paydown date to June 30, 2023.

- Launched Gage branded products in Maryland.

- Partnered with The Hoffman Centers to offer free expungement services in New Jersey.

- Appointed Jeroen De Beijer as Chief People and Culture Officer.

- Launched adult-use cannabis sales at Cookies Detroit retail location.

- Closed on acquisition of high performing and well located dispensary in Maryland.

- Entered into multi-year agreement to introduce Wana’s products at The Apothecarium retail stores and additional third-party retailers in New Jersey and Maryland.

Full Year and Fourth Quarter 2022 Financial Results

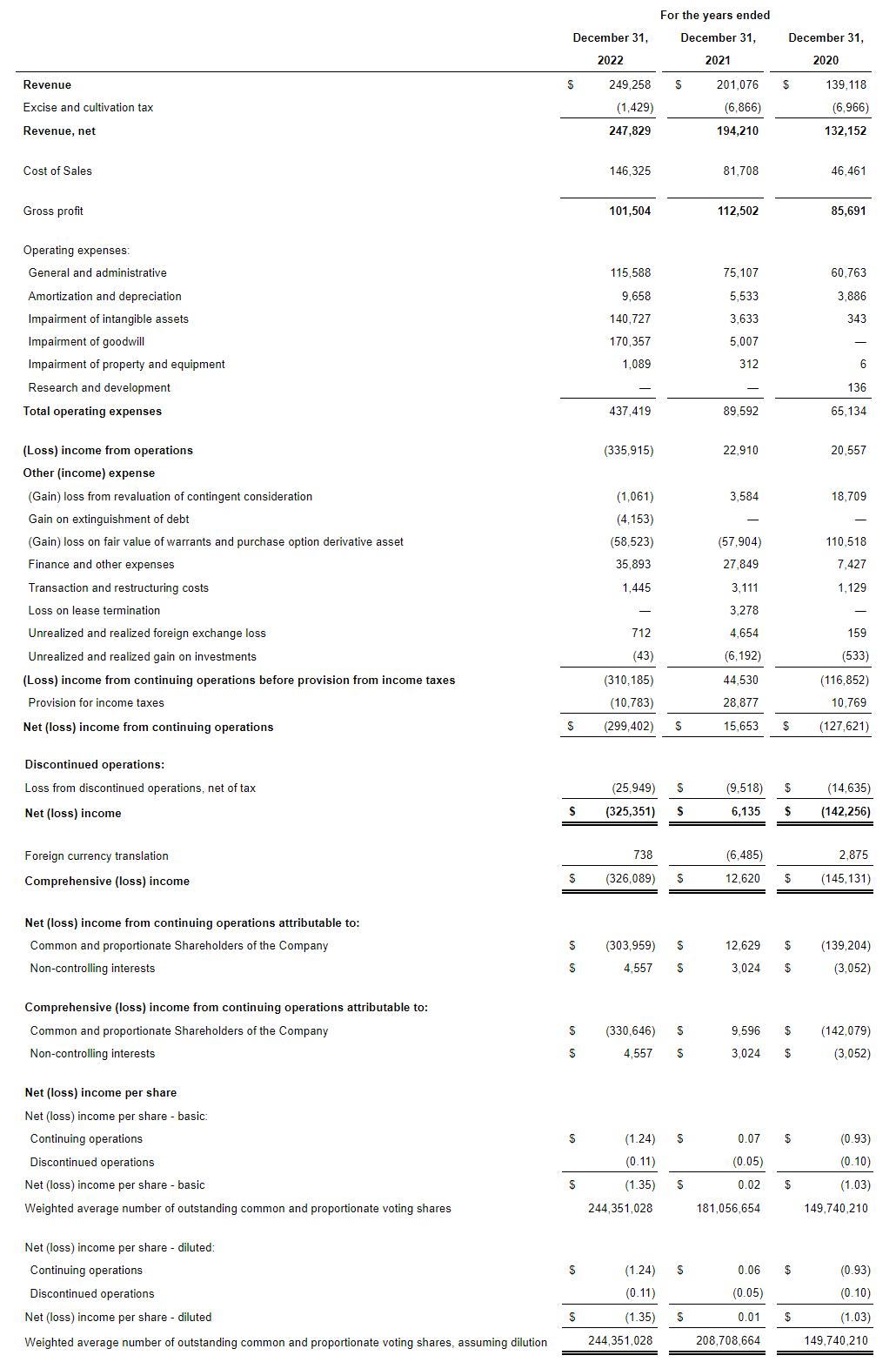

Net revenue for the full year 2022 totaled $247.8 million as compared to $194.2 million for 2021, an increase of 27.6%, primarily driven by the launch of adult use sales in New Jersey and the acquisitions of Gage and Pinnacle in Michigan, partially offset by declines in Pennsylvania.

Net revenue for the fourth quarter of 2022 was $69.0 million as compared to $66.2 million for the third quarter of 2022 and $45.9 million for the fourth quarter of 2021, representing sequential growth of 4.2% and year-over-year growth of 50.3%. The sequential growth was driven by the acquisition of Pinnacle in Michigan, a rebound in Pennsylvania wholesale, and continued growth of adult use sales in New Jersey.

Gross profit margin for the full year 2022 was 41.0% as compared to 57.9% for the full year 2021. Adjusted gross margin, a non-GAAP financial measure, for the full year 2022 was 46.0% compared with 59.9% in 2021. The decline was driven by a reduction in gross margin in Pennsylvania, due to competitive pricing, and the inclusion of Michigan.

Gross margin for the fourth quarter of 2022 was 44.6% as compared to 47.0% in the third quarter of 2022 and 49.1% in the fourth quarter of 2021. Adjusted gross profit margin, a non-GAAP financial measure, was 45.3% for the fourth quarter of 2022 as compared to 47.8% for the third quarter of 2022 and 52.9% for the fourth quarter of 2021. The sequential decline in adjusted gross profit margin was driven by start-up expenses at the Company’s new Hagerstown, Maryland cultivation facility and pricing pressure in Michigan, partially offset by improvement in Pennsylvania.

General & Administrative expenses (G&A) for the full year 2022, excluding stock-based compensation, were $103.4 million as compared to $60.2 million in 2021. The increase in G&A year-over-year was driven primarily by the addition of Michigan, which added $40 million of G&A spend, as well as the conversion to adult use in New Jersey.

G&A for the fourth quarter of 2022, excluding stock-based compensation, were $33.6 million as compared to $24.0 million in the third quarter of 2022 and $15.3 million in the fourth quarter of 2021. The sequential increase was driven by a $10.0 million reserve for bad debt related to a customer in Michigan. Trade receivables on December 31, 2022 were $4.2 million, 96% of which are current, after recording this reserve.

GAAP Net loss from continuing operations for the full year 2022 was $299.4 million compared to net income of $15.7 million in 2021. 2022 includes a $311.1 million non-cash impairment of goodwill and intangibles, as previously disclosed in the results related to the Company’s Michigan reporting unit.

GAAP Net loss from continuing operations in the fourth quarter of 2022 was $2.0 million compared to a net loss from continuing operations of $300.6 million in Q3 2022. Q3 was impacted by the $331.2 non-cash impairment charge previously reported, which was reduced by $20.2 million in Q4 based on the finalization of the fair value of the net assets acquired.

Full year 2022 Adjusted EBITDA from continuing operations, a non-GAAP measure, was $38.8 million as compared to $69.6 million in 2021. The year-over-year decline was driven by competitive conditions in Pennsylvania, partially offset by an increase in New Jersey driven by the conversion to adult use.

Fourth quarter 2022 Adjusted EBITDA from continuing operations, a non-GAAP measure, was $12.2 million, representing a 17.7% Adjusted EBITDA Margin, as compared to $13.0 million and $13.2 million of Adjusted EBITDA from continuing operations and 19.6% and 28.6% of Adjusted EBITDA Margin from continuing operations in the third quarter of 2022 and the fourth quarter of 2021, respectively. The sequential decline in Adjusted EBITDA from continuing operations from the third quarter of 2022 to the fourth quarter of 2022 was driven by pricing pressure in Michigan and start-up expenses at the Company’s Hagerstown facility in Maryland.

Balance Sheet and Cash Flow

Cash and cash equivalents were $26.2 million as of December 31, 2022, compared to $34.2 million as of September 30, 2022. Cash flow from operations grew significantly to a positive $7.3 million for the fourth quarter of 2022 compared to a positive $1.5 million in the previous quarter as a result of the Company’s continued focus on improving cash flow from operations. Capex spending was $13.5 million in the fourth quarter of 2022, primarily related to final payments for the Company’s new Hagerstown, MD cultivation and processing facility, which was completed and became operational in the third quarter of 2022.

During the fourth quarter of 2022, the Company completed a $45.5 million financing with Pelorus Equity Group and paid down $30 million of its $55 million term loan with Chicago Atlantic, refinancing the remaining balance of $25 million. The Company also made a $5 million paydown on its Pennsylvania term loan during the quarter.

As of March 15, 2023 there were 350 million basic shares outstanding including 273 million common shares, 13 million preferred shares as converted, and 64 million exchangeable shares. Additionally, there are 66 million warrants and options outstanding at a weighted average price of $4.29.

Conference Call

TerrAscend will host a conference call today, March 16, 2023, to discuss these results. Jason Wild, Executive Chairman, Ziad Ghanem, President and Chief Operating Officer, and Keith Stauffer, Chief Financial Officer, will host the call starting at 5:00 p.m. Eastern time. A question-and-answer session will follow management’s presentation.

Date: Thursday, March 16, 2023

Time: 5:00 p.m. Eastern Time

RapidConnect URL: https://bit.ly/3iS4NpX

Webcast: Click Here

Dial-in Number: 1-888-664-6392

Conference ID: 95181103

Replay: 416-764-8677 or 1-888-390-0541

Available until 12:00 midnight Eastern Time Thursday, March 30, 2023

Replay Entry Code: 181103#

Financial results and analyses are available on the Company’s website (www.terrascend.com) and SEDAR (www.sedar.com).

The Canadian Securities Exchange (“CSE”) has neither approved nor disapproved the contents of this news release. Neither the CSE nor its Market Regulator (as that term is defined in the policies of the CSE) accepts responsibility for the adequacy or accuracy of this release.

About TerrAscend

TerrAscend is a leading North American cannabis operator with vertically integrated operations in Pennsylvania, New Jersey , Michigan and California , licensed cultivation and processing operations in Maryland and licensed production in Canada . TerrAscend operates The Apothecarium and Gage dispensary retail locations as well as scaled cultivation, processing, and manufacturing facilities in its core markets. TerrAscend’s cultivation and manufacturing practices yield consistent, high-quality cannabis, providing industry-leading product selection to both the medical and legal adult-use markets. The Company owns several synergistic businesses and brands, including Gage Cannabis, The Apothecarium, Ilera Healthcare, Kind Tree, Prism, State Flower, Valhalla Confections, and Arise Bioscience Inc. For more information, visit www.terrascend.com.

Caution Regarding Cannabis Operations in the United States

Investors should note that there are significant legal restrictions and regulations that govern the cannabis industry in the United States. Cannabis remains a Schedule I drug under the US Controlled Substances Act, making it illegal under federal law in the United States to, among other things, cultivate, distribute, or possess cannabis in the United States. Financial transactions involving proceeds generated by, or intended to promote, cannabis-related business activities in the United States may form the basis for prosecution under applicable US federal money laundering legislation.

While the approach to enforcement of such laws by the federal government in the United States has trended toward non-enforcement against individuals and businesses that comply with medical or adult-use cannabis programs in states where such programs are legal, strict compliance with state laws with respect to cannabis will neither absolve TerrAscend of liability under U.S. federal law, nor will it provide a defense to any federal proceeding which may be brought against TerrAscend. The enforcement of federal laws in the United States is a significant risk to the business of TerrAscend and any proceedings brought against TerrAscend thereunder may adversely affect TerrAscend’s operations and financial performance.

Definition and Reconciliation of Non-GAAP Measures

In addition to reporting the financial results in accordance with GAAP, the Company reports certain financial results that differ from what is reported under GAAP. Non-GAAP measures used by management do not have any standardized meaning prescribed by GAAP and may not be comparable to similar measures presented by other companies. The Company believes that certain investors and analysts use these measures to measure a company’s ability to meet other payment obligations or as a common measurement to value companies in the cannabis industry, and the Company calculates Adjusted Gross Profit and Adjusted Gross Profit Margin as Gross Profit and gross profit margin adjusted for certain material non-cash items including the one-time relief of fair value of inventory on acquisition, non-cash write downs of inventory, sales returns and write downs of inventory as a result of a vape recall in Pennsylvania, and other one-time adjustments to gross profit that management does not believe are reflective of ongoing operations. We calculate Adjusted EBITDA from continuing operations and Adjusted EBITDA Margin as EBITDA from continuing operations adjusted for certain material non-cash items such as inventory write downs outside of the normal course of operations, share based compensation expense, impairment charges taken on goodwill, intangible assets and property and equipment, the gain or loss recognized on the revaluation of our contingent consideration liabilities, one-time write off of accounts receivable related to one customer that was deemed uncollectible, loan modification fees related to the modification of debt, the gain recognized on the extinguishment of debt, the gain or loss recognized on the remeasurement of the fair value of the U.S denominated preferred share warrants, one time fees incurred in connection with our acquisitions and certain other adjustments management believes are not reflective of the ongoing operations and performance. Such information is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP. The Company believes this definition is a useful measure to assess the performance of the Company as it provides more meaningful operating results by excluding the effects of expenses that are not reflective of the Company’s underlying business performance and other one-time or non-recurring expenses.

The table below reconciles Gross Profit and Adjusted Gross Profit for the quarters ended December 31, 2022, September 30, 2022, and December 31, 2021:

The table below reconciles net loss from continuing operations to EBITDA from continuing operations and Adjusted EBITDA from continuing operations for the quarters ended December 31, 2022, September 30, 2022, and December 31, 2021: