You’re reading this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news. We no longer send these by email as we did in the past, but we post this and all of the newsletters on our website here.

Friends,

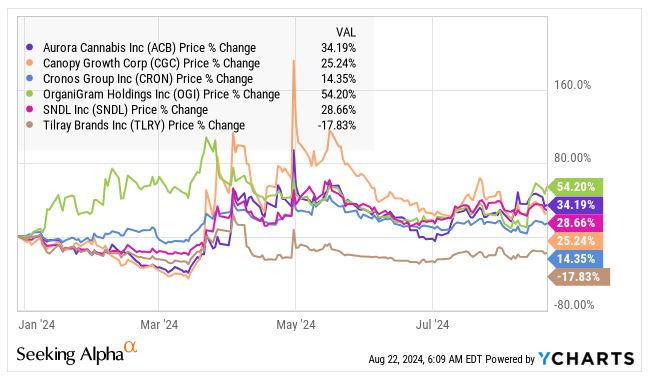

There are six Canadian LP stocks in the New Cannabis Ventures Global Cannabis Stock Index, and they make up 22% of it currently. This is the same exposure as the MSOs, but less than half of the exposure of Ancillaries at 46.5%. Included in the Ancillaries are the 4 REITs, which currently make up 15% of the entire index and about 1/3 of the Ancillary exposure. Here is how those six LPs have performed so far in 2024:

Five of the six are up, and each of them is up more than the index, which is up 10.0% year-to-date. The average return of these six LPs has been a strong 23.2%.

In the model portfolio that I offer at 420 Investor, I have 28.6% exposure to the LPs through three positions. This is up this week, as I added to one name and added back a new name. On 8/16, I was neutral to the index, after having 32% exposure as of 8/16 and 8/9.

Two of the three stocks that I own now are part of the index, and one, my largest position, is not. The stock of Village Farms, up 43% so far in 2024, trades at a significant discount to its tangible book value. Cronos Group, up 14% year-to-date now, is the name that I added this week and is my second-largest LP. It trades just below tangible book value which is mainly its large amount of cash. The smallest position, Organigram, has long been a favorite stock of mine. I reduced it greatly after it rallied following its Q3 earnings report but added some back yesterday at a big discount to where I had reduced. It currently trades at a slight premium to tangible book value.

Cronos Group is not particularly well scaled. It is burning cash and still has negative adjusted EBITDA. My interest in it is mainly due to the discount to tangible book value, the potential for Altria to buy the rest perhaps and opportunities beyond Canada. For now, though, the analysts have negative adjusted EBITDA forecasts for many years ahead.

Organigram, like Cronos Group, has a strategic investor (British American Tobacco) that is actually investing into it by buying stock directly from it at a relatively high price. The balance sheet is already very strong, and the company is doing fairly well in Canada with international opportunities as well. Organgram is already generating positive adjusted EBITDA and trades at an enterprise value to projected adjusted EBITDA for FY25 of 20X, which doesn’t’ stand out as a big bargain. The adjusted EBITDA is expected to grow 57% in FY26 and looks attractive if that estimate stays in place or increases over the next year. It’s not as cheap as when we called it out as a bargain 16 months ago or when we pointed it out down more than 25% year-to-date four months ago, but it looks attractive, especially on a dip.

We don’t publish as much content here on Village Farms due to its smaller size. When I warned in May about the Canadian LPs, it was up 72.1% year-to-date, and it is lower now but still up a lot from its lows. It’s not just a cannabis company, as the largest business is produce. Despite it not being in the index I am trying to beat (and beating!), my model portfolio has a 17.1% stake. The company has no strategic investor like the other two, and it is not debt free like them. Still, the debt level is low and not due very soon. Beyond trading at a 40% discount to its tangible book value, the stock looks attractive relative to the projected adjusted EBITDA. I think that the Canadian LP part of the company alone is worth more than the current valuation. It is up almost 40% since I called it out in April 2023 in this newsletter.

While I am currently overweight the LP sector, I don’t care for all of the LPs. I include Canopy Growth and Tilray on my Focus List and think that both are highly overvalued. I am a bit overweight the sub-sector now. All three stocks that I am long are up a lot, and this worries me a bit. Still, they look cheap to peers. The whole sub-sector would benefit if Canada were to reduce its cultivation tax. Tomorrow, Canada will release its June sales data, and the month may have seen a decline in overall sales for the first time since the country legalized.

I have written positively about the Canadian LPs before, but this tended to be as an alternative to the overly-hot MSOs, which ran up too much and too quickly on the potential rescheduling news. I no longer worry too much about the MSOs and have slightly more exposure to that sub-sector in my model portfolio at 32.4%. Our index that captures the MSOs, the American Cannabis Operator Index, is up only 3.0% in 2024.

I am bullish on some LPs, and I am feeling much more optimistic about all cannabis stocks with potential rescheduling soon. Cannabis investors have a lot of different ways to capitalize on cannabis.

To get real-time updates download our free mobile app for Android or Apple devices, like our Facebook page, or follow Alan on Twitter. Share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

Use the suite of professionally managed NCV Cannabis Stock Indices to monitor the performance of publicly-traded cannabis companies within the day or over longer time-frames. In addition to the comprehensive Global Cannabis Stock Index, we offer the Canadian Cannabis LP Index, the American Cannabis Operator Index and the Ancillary Cannabis Index.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor earnings conference calls.

Discover upcoming new listings with the curated Cannabis Stock IPOs and New Issues Tracker.

Sincerely,

Alan