The year that just ended was one of the most remarkable of the nearly eight that have passed since I began covering the cannabis industry in early 2013. We began 2020 in a tenuous position, as the industry was starving for capital following the vape crisis in late 2019. I had expected this to be a year of big winners (those who had access to capital) and big losers (those who didn’t), but the wild deviations in performance among leading companies was unprecedented.

While the New Cannabis Ventures Global Cannabis Stock Index gained a rather unimpressive 5% overall, indeed there were some very big winners during the year, including names that were included in it at the end of 2019 and some that joined as the year played out. There were also some very big losers, like Harvest Health and Recreation (CSE: HARV) (OTC: HRVSF), iAnthus (CSE: IAN) (OTC: ITHUF) and MedMen (CSE: MMEN) (OTC: MMNFF), three of the leading companies in terms of revenue, as detailed on the New Cannabis Ventures Public Cannabis Company Revenue & Income Tracker, that all saw massive dilution during the year as the they struggled to overcome weak balance sheets.

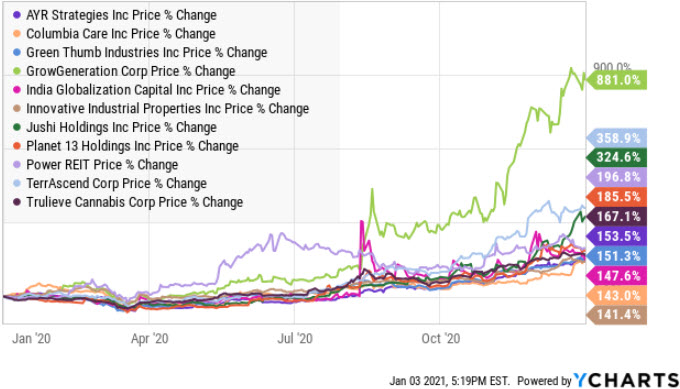

For this article, I have evaluated only names that were part of the Global Cannabis Stock Index as of September 30th. There are many other stocks that more than doubled, but I am not including them here. There were 11 companies in the index during the 4th quarter that ended up doubling or better, or almost 1/3 of the members in the index during during the quarter. Interestingly, at the bottom of the market on March 18th, no stock was better than -21% year-to-date. In fact, four were down more than 50% and ten were down more than 30%. By the end of the year, these 11 stocks returned on average more than 259% with a median return of 167% for the full year:

GrowGeneration (NASDAQ: GRWG): +881%

GrowGeneration leveraged its NASDAQ listing and strong fundamentals to produce a meteoric rise in its price. At the beginning of the year, analysts expected the company to generate revenue of $131 million in 2020. By the end of the year, the forecast rose to $188 million after the company performed better than expected and also closed several large acquisitions. Profit expectations increased substantially as well, with adjusted EBITDA expectations increasing from $13.6 million to $19.2 million. The outlook for 2021 improved even more dramatically over the year. The launch into the stratosphere followed a $48 million equity offering at $5.60 in late June that was very well received by the market. Then, the company blew out expectations when it reported its Q2 in August, which was followed by aggressive trading on the Robinhood platform and a very bullish segment on Mad Money with Jim Cramer. The balance of 2020 saw continued positive news flow, including a strong Q3, a boosted outlook and several acquisitions. GrowGen capped the year with a sale of $172.5 million of stock at $30 per share and then went on to post a new high near $42.

TerrAscend (CSE: TER) (OTC: TRSSF): +359%

TerrAscend was the best performing MSO in 2020, though technically it is more than an MSO given its CBD and Canadian LP operations. The company is one of several operators more narrowly focused by geography, with operations in California and Pennsylvania primarily for most of the year. In addition to becoming operational for the medical cannabis program in New Jersey, which approved adult-use in November, the company also entered Maryland’s medical cannabis market through an acquisition late in the year. Very strong performance in Pennsylvania’s robust market certainly played a major role in the company’s success, but there were several additional factors. First, the company moved to upgrade the management team and consolidate its leadership team in New York City. Additionally, the company was able to access substantial capital from strategic investor Canopy Growth at a very low rate of 6.10% for a very long term. Also, unlike most of the MSOs, TerrAscend began providing guidance for the quarter ahead in May, for 2020 in August and for 2021 in November. Finally, the company had an exceptional investor day in August, its first one, that helped it better connect with investors. Over the balance of the year, it showed very strong growth, with Q3 revenue growing 90% with an adjusted EBITDA margin of 35%.

Jushi Holdings (CSE: JUSH) (OTC: JUSHF): +325%

Jushi Holdings, similarly to TerrAscend, was flying under the radar until it hosted a highly informative investor day on October 1st. The company’s success also came from a relatively narrow geographical footprint that it expanded during the year with an investment into Virginia ahead of its medical cannabis program commencing sales to patients late in the year. It was able to use M&A to boost its vertical integration in Pennsylvania, where it had a strong retail presence but needed more supply. Jushi priced a large debt deal with warrants in February and followed up with another one in July. By the end of the year, it not only raised additional capital through an equity offering, but it also was able to boost its cash balances by accelerating the expiration date of the warrants issued earlier in the year. Jushi provided 2021 guidance early in the year for revenue and later shared its adjusted EBITDA outlook. At its investor day, it boosted its outlook and provided a detailed state-by-state forecast of how it expected to achieve 2021 revenue of $205-255 million, a gain of at least 197% above projected 2020 revenue.

Power REIT (NYSE: PW): +197%

Power REIT began to focus more aggressively on the cannabis industry in early 2020 after acquiring its first greenhouse properties for sale-leaseback in 2019. Its operational focus includes the broader controlled environment agriculture (greenhouses) as well as solar farm land and railroad property, its legacy operations. The company has properties in Maine and Colorado. Unlike Innovative Industrial Properties, it isn’t focused on MSOs. Power REIT reports that 2/3 of its revenue and half its assets are from greenhouses. Its success, then, appears to be a successful shift in its business model that was likely helped by its higher exchange listing as well as its relatively small market capitalization.

Planet 13 Holdings (CSE: PLTH) (OTC: PLNHF) + 185%

Given its 100% operational exposure during the year to Las Vegas, it took an incredible effort by Planet 13 to overcome the obstacles of the pandemic. Management here, which is led by its founders, adapted to the changing market quickly, pivoting to serve the local market through delivery. In Q3, despite the pandemic, it grew revenue 37% compared to a year ago. It purchased a second production facility and was able to win a settlement with the state that allowed it to open a second dispensary in Las Vegas, and it also aggressively stepped up its own production capabilities for internal sale as well as wholesale. After renegotiating a deal to acquire a license in Orange County, California in its favor, it moved forward on its development plans to open its second superstore and expand its geographical footprint. The company was able to raise equity three separate times in the second half of the year, maintaining a strong, debt-free balance sheet.

Trulieve (CSE: TRUL) (OTC: TCNNF): 167%

Trulieve entered the year as essentially a single-state operator in Florida but the one with the most revenue and by far the most profitable cannabis operator. Its success in 2020 was due to very strong execution in Florida, a market that exhibited very strong growth in patient count of about 52% during the year. Additionally, the company was able to make a meaningful expansion into another state at a seemingly reasonable price as it purchased two companies in Pennsylvania. The rise in the price of its stock was due to better than expected growth in Florida, the acquisitions and multiple expansion, as it ended the year trading at 5X projected 2021 revenue after beginning the year trading at 2.8X projected 2020 sales.

Ayr Strategies (CSE: AYR.A) (OTC: AYRWF): +154%

Ayr Strategies didn’t begin the year as a leading MSO, but it ended 2020 with a market cap above $1 billion as it moved from a two-state operator to one that will be in seven states, pending the close of several acquisitions. Like Planet 13, with operations in the tourist-centric Nevada market as well as in Massachusetts, where adult-use was shut down, the company was able to stand up to tremendous challenges. Investors were pleased with the company’s ability to remain profitable in Q2, even as revenue was pressured. Compared to Q1, revenue dropped 16% but adjusted EBITDA expanded by 8% as the company’s adjusted EBITDA margin reached 32%. As growth returned in Q3, with revenue increasing 61% sequentially, its adjusted EBITDA margin soared to 42%. In addition to reasonably priced deals to enter Pennsylvania, Ohio, Arizona and, later, New Jersey and Florida, the company scored a major victory in Massachusetts by securing host community agreement approvals for three dispensaries for adult-use in greater Boston.

Green Thumb Industries (CSE: GTII) (OTC: GTBIF): +151%

Green Thumb Industries, which added 1300 employees during the year, was the first MSO to surpass $100 million quarterly revenue, a feat that it accomplished in Q2. The company began the year trading at 3.8X projected 2020 revenue of $474 million. Analysts now expect 2020 revenue to have been $549 million, so better than expected organic growth, primarily in Illinois and Pennsylvania, was certainly a major factor. Based on 2021 projected revenue of $841 million, GTI is trading at 6.5X forward sales, illustrating how higher valuation accounted for a large portion of the company’s gains. Looking at adjusted EBITDA suggests multiple expansion was less of a factor. The stock was valued at 14X projected 2020 adjusted EBITDA at the beginning of the year and now trades at 18.6X projected 2021 adjusted EBITDA. In addition to strong growth in revenue and profitability and solid execution, the company was able to attract investment from an unnamed institutional investor that purchased shares just ahead of the election and then again at a substantially higher price afterwards.

India Globalization Capital (NYSE American: IGC): +148%

It’s difficult to understand why investors chased India Globalization Capital, as it has very poor fundamentals. It seems that the company benefited solely from its exchange listing and low price that appealed to speculators.

Columbia Care (CSE: CCHW) (NEO: CCHW) (OTC: CCHWF): +143%

With a big footprint but lagging financials compared to its peers, Columbia Care flew under the radar for most investors for most of 2020. Closing the acquisition of The Green Solution, a large Colorado operator, in early September and then announcing and closing an acquisition in California changed the perceptions of the company. Not only did it show that it could buy quality assets at good prices, the acquisitions helped address the perceived weakness to the story that it wouldn’t be able to compete in adult-use markets. Another smart M&A transaction was announced later in the year, the pending acquisition of Green Leaf Medical, a private MSO operating in four mid-Atlantic states. Again, the company got what looks like a great deal, but it also appears to be a synergistic transaction. Another potential driver of the stock price was a very late move to dual list on the Canadian Securities Exchange, which is more oriented towards retail investors. Jushi and Ayr Strategies were much quicker to recognize the importance of retail investors, moving from the NEO, where they had originally listed, to the CSE. Finally, the company exhibited capital markets prowess, issuing debt capital and accessing additional capital through sale-leaseback transactions as well as an impressive monetization of its international operations. So, a combination of factors, including what looks like very smart M&A but also a cheap valuation (the stock still trades below peers at 4X projected 2021 revenue), were primarily responsible for Columbia Care’s impressive performance.

Innovative Industrial Properties (NYSE: IIPR): +141% (+151% with dividends)

Cannabis REIT Innovative Industrial Properties was in the perfect spot in 2020, as even the best capitalized cannabis companies chose to turn to it rather than sell equity or take on debt for most of the year. The company raised capital at progressively higher prices and deployed it aggressively. It raised $250 million in January at $73.25, $115 million at $74.16 in May, and $259 million at $83.85 in July in underwritten offerings, and it also raised $141 million through its “at-the-market” equity offering program at approximately $94.20. During the year it added additional clients, diversifying its customer base, but it also deepened its relationships with many of its existing clients. Its revenue and profits soared during the year, allowing it to boost its dividend 24% over the year-ago level.

Some Takeaways From 2020 and Thoughts About the Year Ahead

Indeed, this was a remarkable year. For the first time, several companies delivered in a big way on the promise of the industry fundamentally, as strong revenue levels and growth as well as profitability were key themes driving the returns of many of these stocks. In the past, gains have been based more on speculation about the future. I am encouraged by where the industry is as we exit 2020 and expect to be writing a similar article a year from now, describing several of 2021’s triple-digit gainers.

I learned a big lesson this year with several of these stocks: They can do much better than I expect. The best example was GrowGeneration, and clearly I wasn’t alone, as insiders and institutional investors were heavy sellers before the stock exploded to levels few imagined could be reached. In April, I shared an extensive review of the company’s 2019 fundamentals and a very bullish outlook with my subscribers at 420 Investor, suggesting the stock could end the year at $7.35 based on obtaining a multiple of 20 times its projected 2021 adjusted EBITDA. It seemed like a stretch at the time, as the target offered 75% return over less than 9 months. Whoops! Similarly, I had a very big position in TerrAscend in my model portfolios at 420 Investor but moved to the sidelines due to my concerns about how they might need to issue equity to fund an earnout, an issue they handled with minimal dilution.

Another important lesson from 2020 is that being on a higher exchange is a major positive. The largest Canadian LPs performed very well around the elections despite having no clear path to benefiting from state legalizations or even any change in the leadership at the federal level. Among the 11 companies discussed here, 4 trade on higher exchanges. This leaves me optimistic that over time, perhaps this year, the state-legal operators may benefit from being able to uplist from the OTC.

Finally, the fact that many of these companies were flying under the radar as the year began is an important reminder to not focus exclusively on the largest companies. At the beginning of the year, investors characterized the MSO landscape as being dominated by just four companies, including GTI and Trulieve as well as Cresco Labs (CSE: CL) (OTC: CRLBF) and Curaleaf Holdings (CSE: CURA) (OTC: CURLF), both of which had great years on all levels but didn’t double in price. Instead, names like Ayr Strategies, Columbia Care, Jushi Holdings, Planet 13 Holdings and TerrAscend, all less followed early in the year by analysts and investors, were able to accomplish that achievement. We explained why there isn’t a winner-take-all environment in the U.S. in July, so we weren’t surprised to see the emergence of several companies that investors began to better appreciate. The number of MSOs with market capitalization in excess of $1 billion expanded from four to nine in 2020.

As I look ahead, I expect that many of the stocks that potentially double in 2021 will surprise investors too. I think that there are some under-the radar companies operating in the U.S. as well as in Canada, where investors don’t seem to recognize some exceptional valuations being offered, that will make the list a year from now. I also expect M&A to play a huge role in 2021, and those companies that can put together smart deals may surprise investors with returns during the year that don’t necessarily seem realistic today based on just the current operations. Finally, we have discussed the role that AdvisorShares Pure U.S. Cannabis ETF (NYSE Arca: MSOS) is likely to play this year (especially on smaller stocks), and there are also institutional investors increasingly participating in the market. This continued broadening of the investor base is helpful, but what could really spawn large gains for American operators would be the ability to trade on higher exchanges.